The 2026 stablecoin landscape

Stablecoins have transitioned from speculative retail instruments to foundational institutional infrastructure. This shift is not merely a change in user demographics but a structural evolution driven by regulatory clarity and the tokenization of real-world assets (RWA). In 2026, stablecoins serve as the primary settlement layer for cross-border payments and collateralized lending, replacing legacy correspondent banking networks in many high-volume corridors.

The passage of the GENIUS Act in the United States established the first comprehensive regulatory framework for "permitted stablecoin issuers." This legislation mandates strict reserve requirements and regular attestations, effectively separating compliant stablecoins from unbacked digital tokens. For institutional capital, this regulatory certainty removed the primary barrier to entry: counterparty risk. Banks and asset managers can now integrate stablecoin rails into their treasury operations with the same confidence they apply to traditional money market funds.

Reserve composition has also matured. Early stablecoins relied heavily on commercial paper and unsecured corporate debt. Today, leading issuers hold the majority of their reserves in short-term U.S. Treasury bills and cash equivalents. This shift aligns the stablecoin ecosystem with traditional financial stability standards, ensuring that the digital dollar remains pegged not by algorithmic faith, but by liquid, regulated government debt.

The rise of RWA tokenization further cements this utility. As trillions of dollars in private credit, real estate, and bonds move on-chain, stablecoins provide the necessary liquidity to settle these transactions instantly. They are no longer just a bridge to crypto; they are the bridge between traditional finance and the programmable economy.

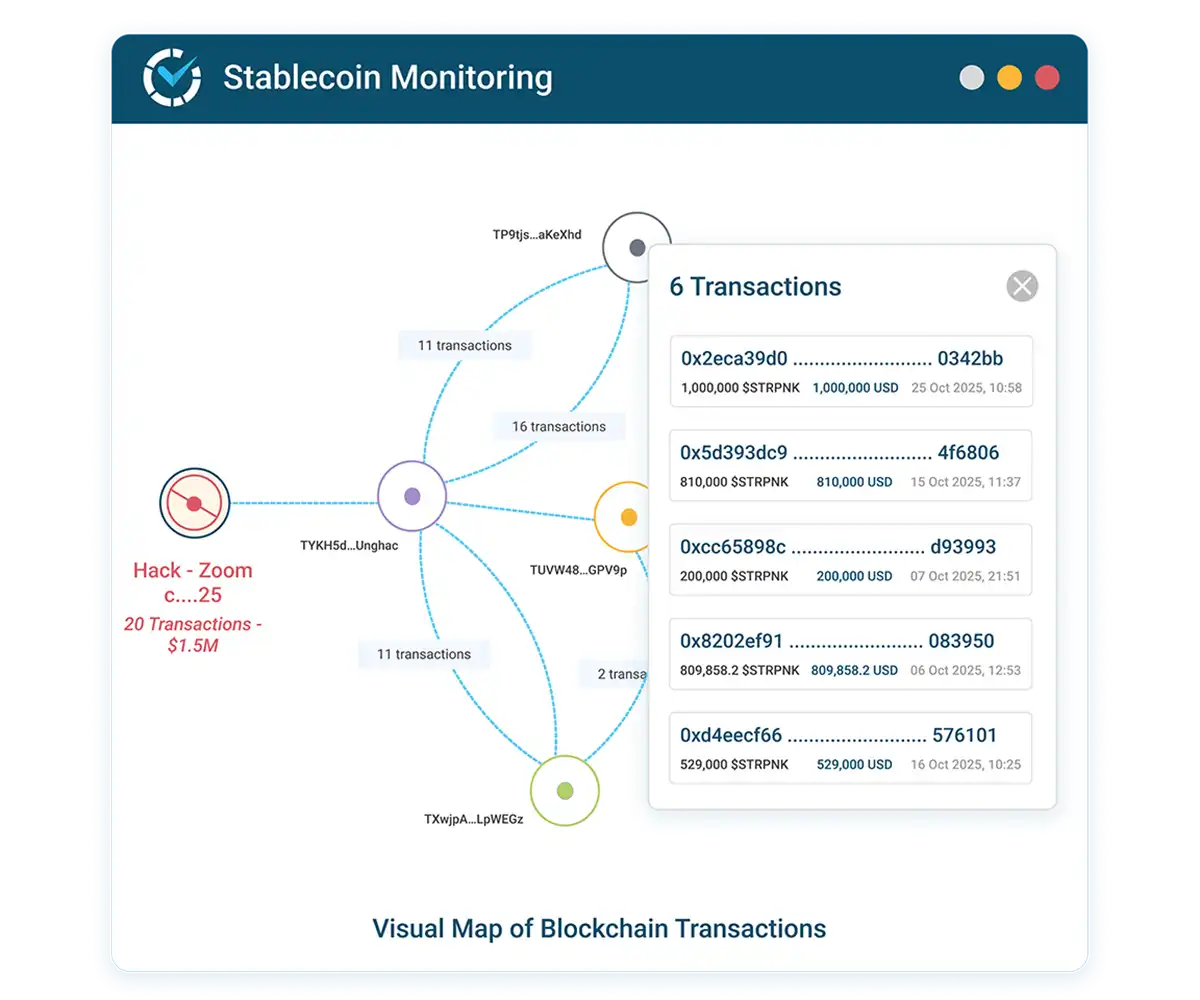

Chart: USDT/USDT price stability and volume trend, reflecting institutional holding patterns rather than speculative trading.

USDC vs USDT market share 2026

The stablecoin duopoly has settled into a clear functional split. Tether (USDT) retains the crown for trading volume and emerging market liquidity, while Circle’s USDC has captured the institutional mandate through regulatory clarity and reserve transparency. Understanding this divergence is essential for navigating capital flows in 2026.

USDT remains the backbone of global crypto trading. Its dominance is driven by deep liquidity on major exchanges and widespread adoption in regions with volatile local currencies. For traders and cross-border remitters in emerging markets, USDT is often the default bridge asset, prioritizing accessibility and speed over the compliance frameworks that define USDC’s value proposition.

Conversely, USDC has positioned itself as the institutional standard. Circle’s strict adherence to US regulations, regular attestation reports, and 1:1 backing with short-dated US Treasuries have made it the preferred vehicle for traditional finance (TradFi) integration. This compliance-first approach has attracted significant inflows from institutional investors seeking to integrate real-world assets (RWA) and stable yield into their portfolios without regulatory ambiguity.

The following table compares the core metrics defining their respective market positions.

| Metric | Tether (USDT) | Circle (USDC) |

|---|---|---|

| Market Cap | ~$110B | ~$40B |

| Primary Use Case | Trading & Emerging Markets | Institutional & Payments |

| Reserve Composition | US Treasuries & Cash | US Treasuries & Cash |

| Regulatory Status | Offshore / Mixed | US-Compliant |

As global stablecoin regulations mature in 2026, the gap between these two models may narrow. However, the current market structure rewards USDT’s liquidity network effects and USDC’s institutional trust. Capital allocation decisions now depend less on which coin is "better" and more on whether the use case prioritizes trading volume or regulatory safety.

Cross-border payments and RWA tokenization

The narrative around stablecoins has shifted from retail speculation to institutional utility. In 2026, the focus is on practical application: moving liquidity across borders faster and under tighter regulatory frameworks, and using digital dollars as collateral in tokenized markets. This transition marks a move from theoretical potential to operational reality.

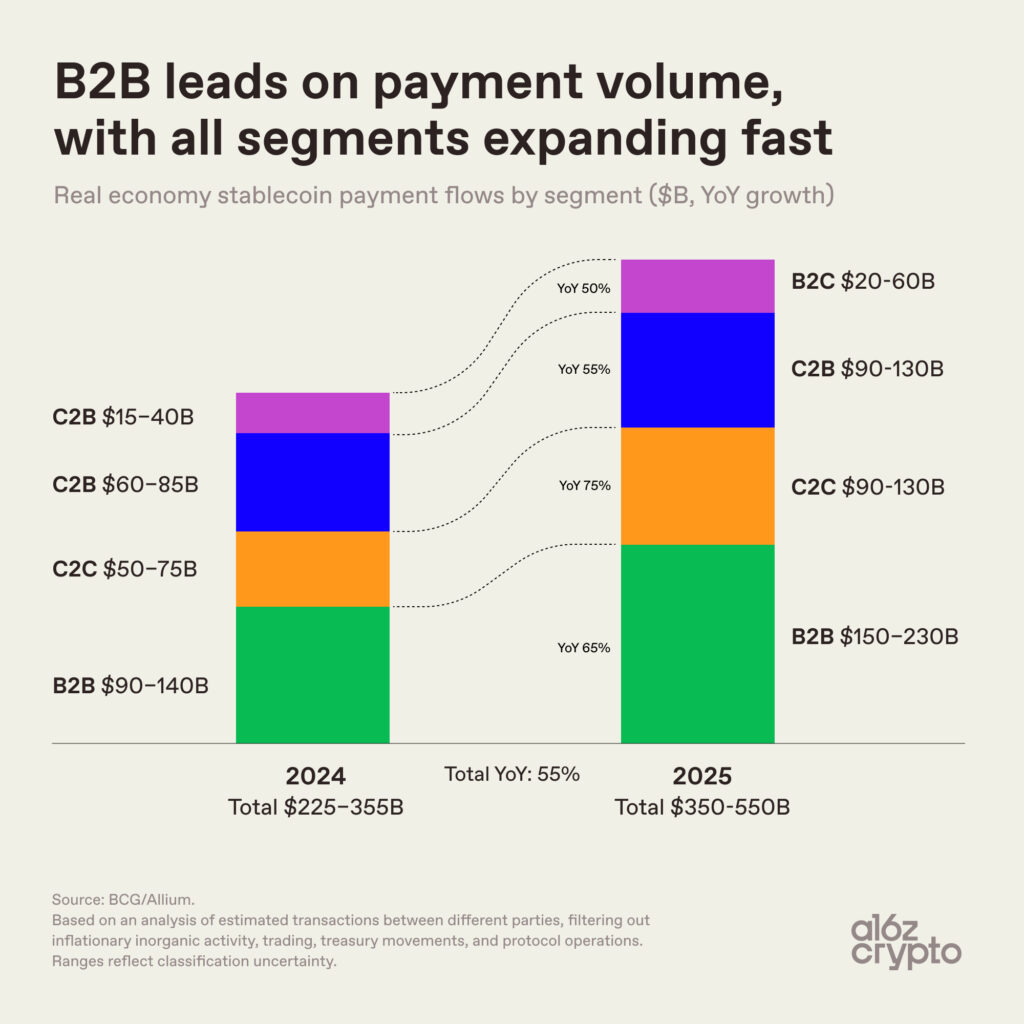

B2B Payments and Cross-Border Efficiency

Stablecoins are increasingly used for business-to-business (B2B) payments, offering a faster and cheaper alternative to traditional wire transfers. While stablecoins remain approximately 1% of global payment flows, the absolute volume is growing exponentially, signaling an early adoption phase among enterprises seeking efficiency. This growth is driven by the need for real-time settlement and reduced intermediary costs in international trade.

The infrastructure supporting these payments has matured, with providers integrating compliance tools and fiat on-ramps. This allows corporations to leverage blockchain technology without sacrificing regulatory oversight. The result is a streamlined payment rail that competes directly with legacy banking systems on speed and cost.

Tokenized Treasuries and RWA Collateral

Real World Assets (RWA) tokenization represents another major pillar of institutional adoption. RWA refers to tangible assets, such as government bonds or real estate, that are represented on a blockchain. Tokenized treasuries, in particular, have gained traction as institutions seek yield on idle cash while maintaining liquidity.

Stablecoins are increasingly used as collateral in these tokenized treasury markets. This creates a closed-loop system where digital dollars can be lent, borrowed, and used as security for tokenized assets. This integration deepens the utility of stablecoins beyond simple transfers, embedding them into the broader financial ecosystem.

The combination of efficient cross-border payments and tokenized asset markets creates a robust foundation for institutional capital. As regulatory clarity improves, these use cases are expected to expand, further cementing stablecoins as a critical component of modern finance.

Regulatory drivers reshaping liquidity

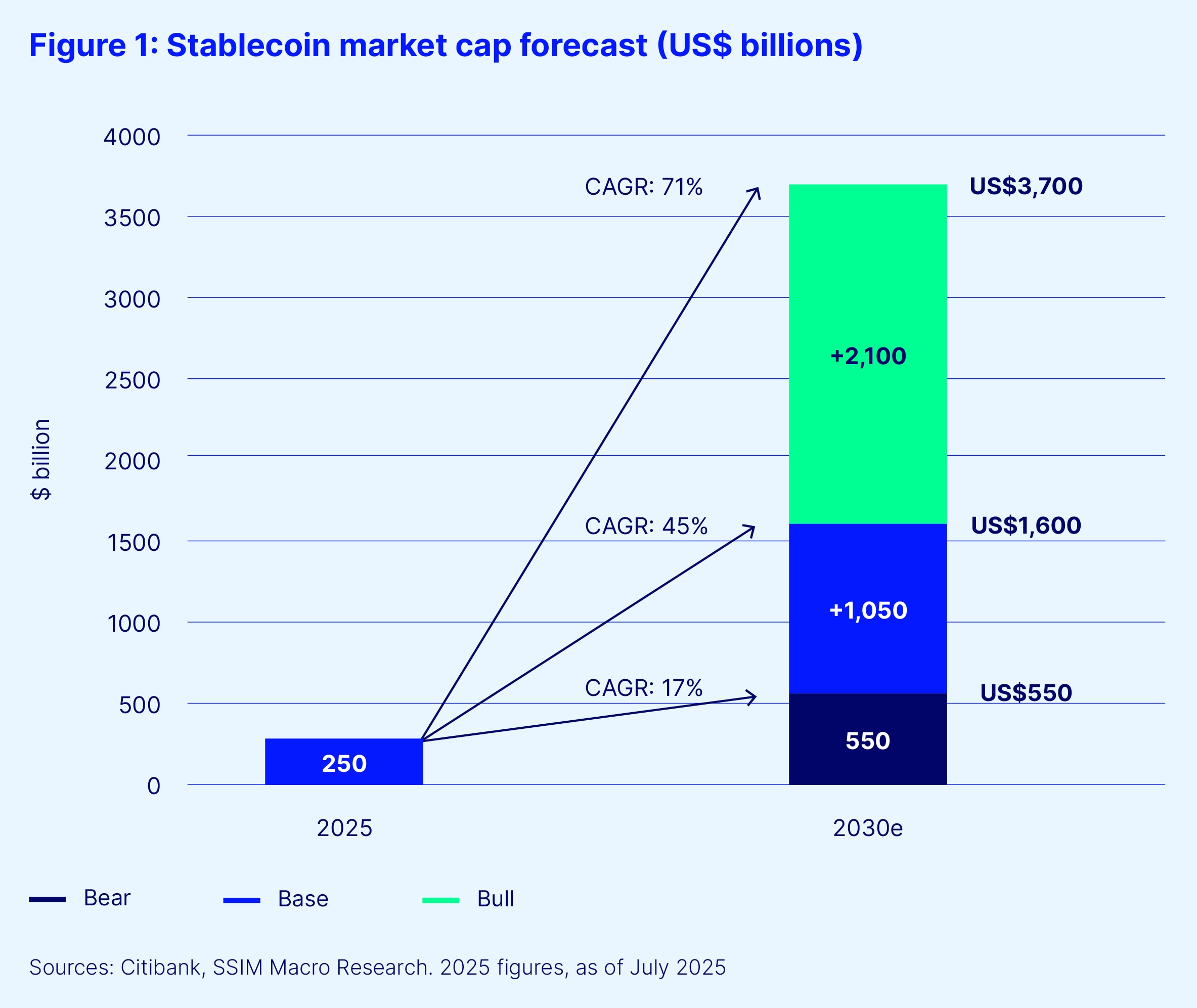

New regulations are no longer just compliance hurdles; they are the primary engine driving stablecoin reserves into traditional government debt. The United States GENIUS Act and the European Union’s MiCA framework have effectively ended the era of speculative reserve management for major issuers. By legally defining "permitted stablecoin issuers," these laws mandate that reserves be held in high-quality, liquid assets, primarily US Treasuries and cash deposits.

This shift has transformed stablecoins from retail speculation tools into institutional utility instruments. Issuers are now forced to hold higher quality reserves, meaning billions in capital are flowing directly into US debt markets. This creates a direct link between crypto adoption and traditional Treasury demand, pressuring banks to adapt their custody and settlement services to handle this new asset class.

The concentration of these reserves introduces new systemic dynamics. As noted by Stripe, large-scale stablecoin adoption could shift deposits away from traditional banks, concentrating liquidity in a few key financial institutions. This feedback loop means that regulatory clarity is not just stabilizing the crypto market, but actively reshaping the broader financial landscape by integrating digital payments with sovereign debt.

Risks to Institutional Adoption

While stablecoins are gaining traction as a settlement layer, their rapid growth introduces structural vulnerabilities that institutional treasurers must weigh against efficiency gains. The primary concern is not market volatility, but rather the mechanics of reserve backing and the potential for systemic feedback loops.

Reserve Concentration and Bank Deposits

The most immediate risk lies in the composition of stablecoin reserves. Many issuers hold a significant portion of their backing in short-term U.S. Treasury bills or commercial bank deposits. As noted by Stripe’s 2026 business trends analysis, large-scale adoption could shift trillions in deposits away from traditional banks, concentrating liquidity in a few key financial institutions.

This dynamic creates a feedback loop: if confidence in a major stablecoin issuer wavers, the simultaneous redemption of reserves could force a fire sale of Treasuries or drain bank deposits, potentially destabilizing the broader banking sector. For institutional users, this means counterparty risk is no longer just about the token’s peg, but about the health of the underlying reserve managers.

Regulatory Fragmentation

Beyond reserve mechanics, the lack of a unified global regulatory framework poses a significant operational hurdle. Institutions operating across borders face a patchwork of compliance requirements, from the EU’s MiCA to varying U.S. state-level money transmitter laws. This fragmentation increases legal costs and complicates cross-border liquidity management, potentially limiting the utility of stablecoins for global treasury operations until clearer harmonization emerges.

No comments yet. Be the first to share your thoughts!