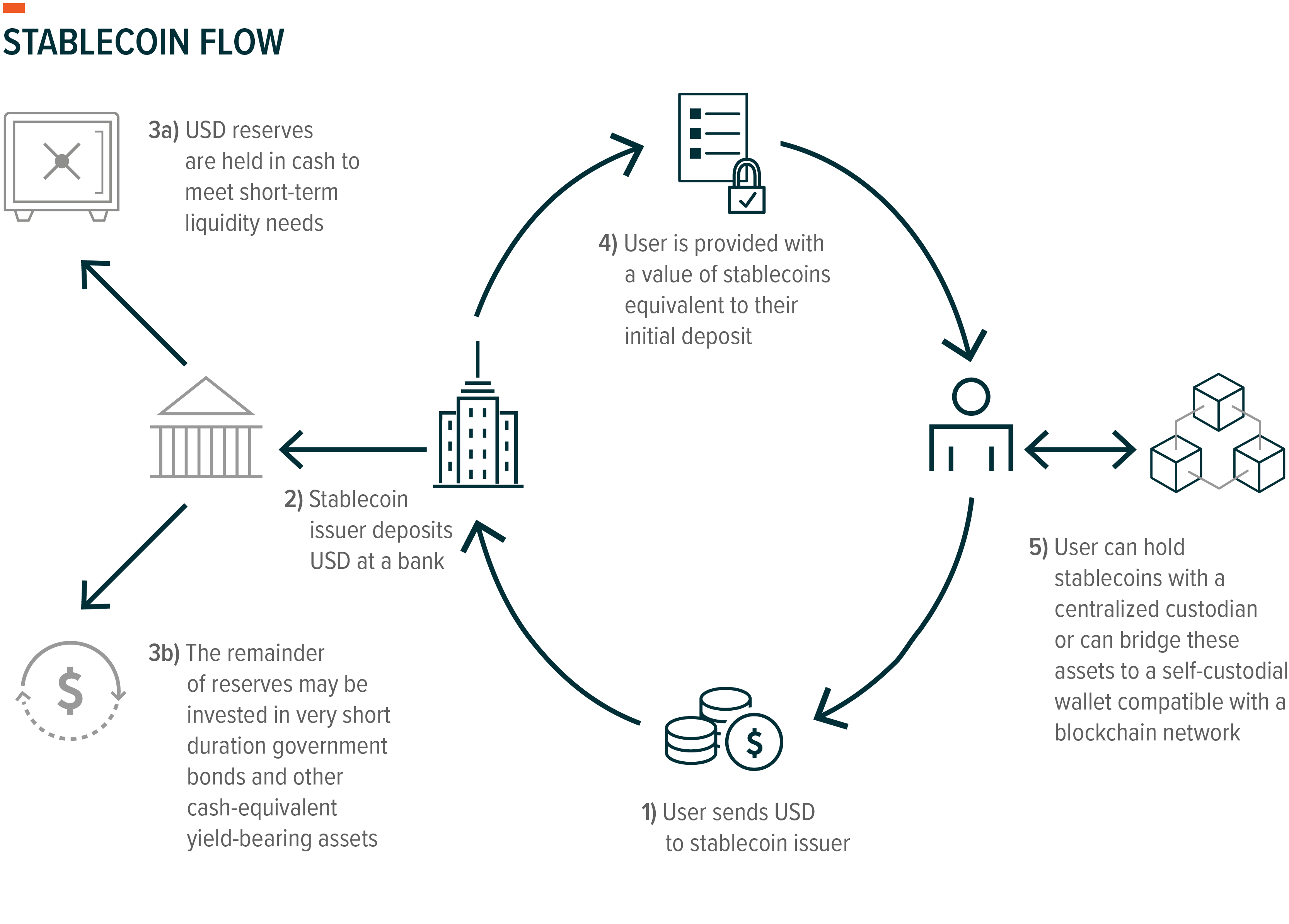

Stablecoin flows shift toward real-world assets

The narrative surrounding stablecoins is undergoing a structural correction. In previous cycles, growth was driven almost entirely by speculative trading volume within crypto-native ecosystems. By 2026, that dynamic has inverted. Stablecoin flows are no longer just about crypto speculation; they are being redefined by real-world asset (RWA) tokenization and institutional liquidity adoption.

This shift marks a transition from digital gold to digital infrastructure. Major payment processors and financial institutions are integrating stablecoins not for arbitrage, but for settlement. As noted by industry analyses from Stripe and Thunes, the primary utility of stablecoins in 2026 is their ability to move liquidity across borders faster and under tighter regulatory compliance frameworks than traditional correspondent banking. This utility-driven demand creates a more stable floor for stablecoin market capitalization, decoupling it from the volatility of underlying crypto assets.

The volume of stablecoins backing tokenized treasuries, real estate, and private credit is expanding rapidly. This integration requires robust compliance layers, driving the adoption of regulated stablecoin issuers. The result is a market where liquidity is increasingly tethered to tangible economic output rather than pure market sentiment.

The chart above illustrates the recent trading volume of Tether (USDT), a proxy for the broader stablecoin liquidity pool. The sustained volume levels, distinct from the sharp spikes seen during speculative manias, reflect the steady, institutional-grade flow of capital into and out of these digital instruments. This baseline activity supports the thesis that stablecoins are becoming a foundational layer for global payments and asset tokenization.

USDC vs USDT market share dynamics

The stablecoin landscape in 2026 is defined by a distinct bifurcation between regulatory compliance and network liquidity. Circle’s USDC and Tether’s USDT remain the dominant forces, yet their competitive advantages serve different segments of the financial ecosystem. USDC has consolidated its position as the preferred instrument for institutional liquidity and regulated on-chain activity, while USDT retains significant volume in cross-border payments and emerging markets.

This divergence reflects broader trends in stablecoin flows. Regulatory clarity has incentivized institutional capital to favor USDC’s transparent reserve structure and US-based compliance framework. Conversely, USDT’s first-mover advantage and deep liquidity across multiple blockchains continue to drive its adoption in high-volume, non-institutional transaction flows.

The following comparison outlines the structural differences that define their respective market positions.

| Feature | USDC | USDT | 2026 Impact |

|---|---|---|---|

| Regulatory Status | US-regulated, fully compliant | Offshore, evolving compliance | USDC leads in institutional adoption |

| Reserve Transparency | Monthly attested reports | Quarterly attested reports | USDC preferred for risk-averse capital |

| Primary Use Case | Institutional DeFi, RWA tokenization | Cross-border payments, retail trading | USDT dominates global transaction volume |

| Market Capitalization | ~$45 billion | ~$120 billion | USDT retains broader liquidity depth |

Market data indicates that while USDT maintains a larger overall market capitalization, USDC’s growth rate is accelerating within regulated financial corridors. The following widget reflects the current valuation dynamics of these assets.

RWA tokenization drives institutional liquidity

Tokenizing real-world assets (RWA) creates a direct bridge between traditional finance and stablecoin networks. By converting bonds, real estate, and private credit into digital tokens, institutions gain the ability to settle transactions instantly while maintaining regulatory compliance. This shift transforms stablecoins from speculative trading instruments into essential infrastructure for global liquidity.

The mechanism is straightforward: an asset is tokenized on a blockchain, and stablecoins serve as the settlement layer. This eliminates the friction of traditional clearinghouses, reducing settlement times from days to seconds. As a result, demand for stablecoins grows not from retail speculation, but from institutional necessity. The liquidity previously trapped in illiquid assets becomes accessible, moving through stablecoin rails with greater efficiency.

OpenFX’s 2026 report highlights a $10T liquidity opportunity across four regions, driven by this convergence of RWA and stablecoin utility. The report notes that stablecoin volume reached $27.6T in Q1 2026, with cross-border payments and treasury products leading the charge. This volume reflects a broader trend: stablecoins are becoming the preferred medium for settling tokenized assets.

Regulatory frameworks are accelerating this adoption. New global rules are reshaping payments by clarifying the status of stablecoins as legitimate settlement assets. The UK, for example, is finalizing its own framework to align with these standards, ensuring that tokenized assets can move freely across borders. This regulatory clarity reduces risk for institutions, encouraging them to integrate stablecoins into their core operations.

The shift from speculation to utility is evident in the data. Stablecoin flows are increasingly tied to real-world economic activity, such as trade finance and cross-border payments. This trend is reinforced by the integration of AI-powered agents and decentralized tools, which help businesses make smarter decisions and operate more efficiently. As a result, stablecoins are becoming a critical component of the global financial infrastructure.

Regulation reshapes cross-border payment rails

The regulatory landscape for stablecoin flows in 2026 has shifted from theoretical debate to enforceable compliance. In Europe, the Markets in Crypto-Assets (MiCA) regulation has established a uniform framework for asset-referenced and e-money tokens, forcing issuers to maintain strict reserve requirements and transparency. This legal clarity has reduced counterparty risk, allowing institutional treasuries to integrate stablecoins into B2B payment rails with confidence previously reserved for traditional correspondent banking.

In the United States, legislative movements have mirrored this trend toward standardization. While a comprehensive federal stablecoin bill remains in progress, executive actions and Treasury guidance have clarified anti-money laundering (AML) expectations for digital asset service providers. These developments are pressuring the industry to adopt standardized reporting protocols, effectively bridging the gap between decentralized finance and regulated financial institutions.

The convergence of these frameworks is accelerating adoption in cross-border settlements. As noted by industry analysts, new global rules are reshaping payments by prioritizing utility over speculation. This regulatory certainty is driving demand for US debt-backed stablecoins, as institutions seek yield-bearing assets that comply with both domestic and international auditing standards. The result is a more robust infrastructure for international liquidity, where compliance is embedded in the protocol rather than treated as an afterthought.

| Region | Key Framework | Primary Impact on Stablecoin Flows |

|---|---|---|

| European Union | MiCA | Uniform reserve requirements and issuer licensing, reducing cross-border friction. |

| United States | Treasury Guidance & State-Level Laws | Clarified AML/KYC obligations, encouraging institutional custody solutions. |

| United Kingdom | Finalizing Framework | Aligning with global standards to remain competitive in digital finance. |

This standardization is not merely bureaucratic; it is a market imperative. As stablecoin flows become integral to global trade, the ability to trace and audit transactions in real-time is becoming a prerequisite for banking partners. The 2026 regulatory environment is effectively filtering out non-compliant actors, leaving a consolidated market of issuers who can support the high-volume, low-latency demands of modern B2B commerce.

No comments yet. Be the first to share your thoughts!