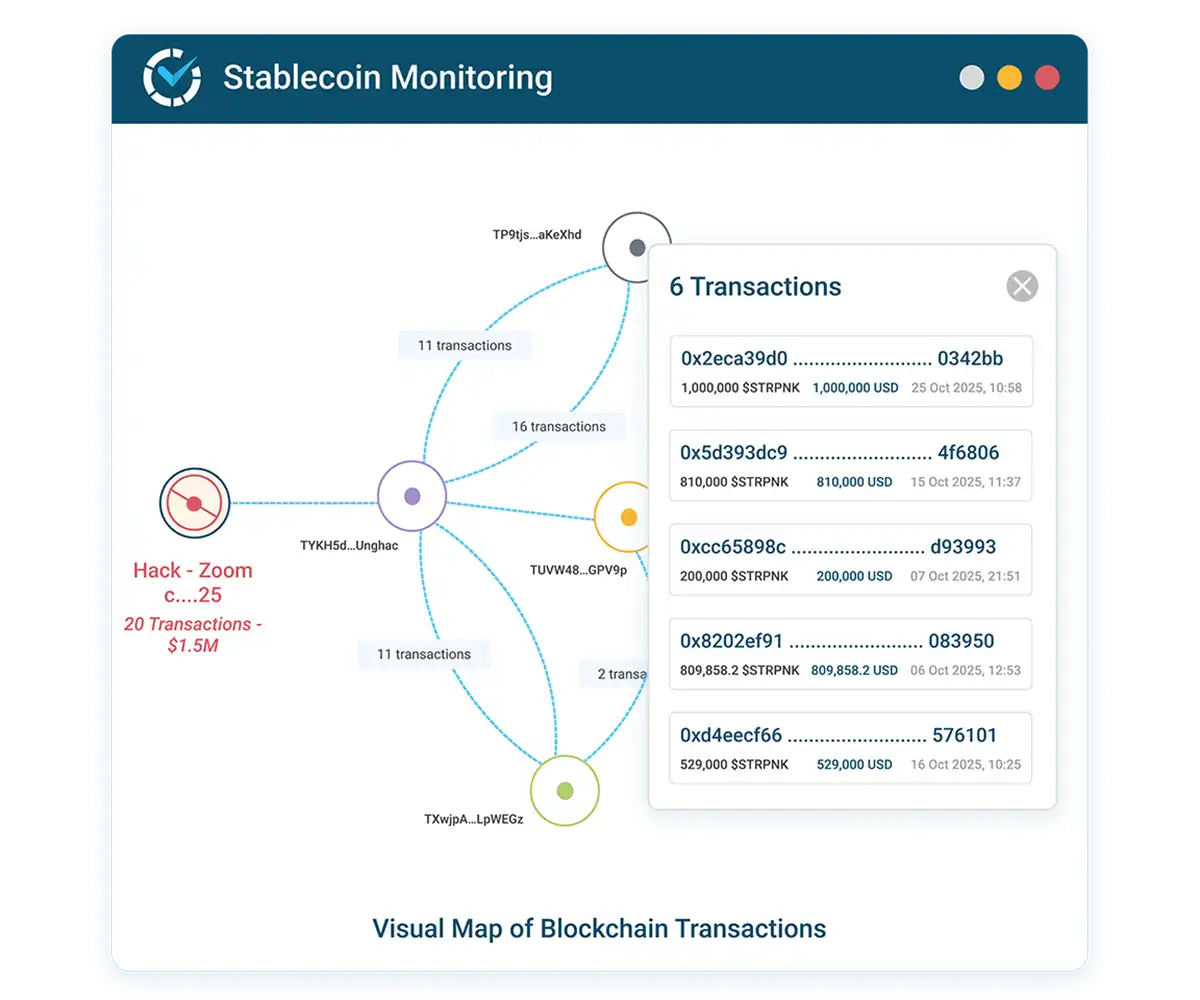

Stablecoin supply holds near $270B

Total stablecoin supply remained steady near $269–270 billion as of mid-January 2026, marking a period of consolidation after years of rapid expansion. This baseline figure reflects a market that has matured beyond the speculative frenzy of previous cycles, settling into a utility-driven rhythm. The dominance of Tether (USDT) continues to anchor the sector, while USDC maintains its position as the preferred instrument for institutional liquidity and regulatory-compliant settlements.

The shift from pure speculation to functional utility is evident in holder behavior. According to recent industry data, half of stablecoin holders increased their positions over the last year, with more than half planning to acquire additional units in the near term. This accumulation pattern suggests that stablecoins are increasingly viewed as a foundational layer of digital cash rather than a temporary parking spot for crypto gains.

To visualize this steady growth trajectory and current market depth, the chart below tracks total stablecoin supply over the last 12 months, highlighting the resilience of the $270B+ ecosystem.

While Bitcoin often serves as the primary reference point for broader crypto sentiment, the stablecoin market operates with distinct mechanics. Its stability is not derived from price appreciation but from its function as a bridge between traditional finance and digital assets. As institutional adoption deepens, the flow of capital through these pegged assets will likely dictate the liquidity conditions for the entire digital asset landscape.

USDC vs USDT market share dynamics

Stablecoin supply held steady near $270 billion in early 2026, with USDT and USDC capturing the vast majority of this liquidity. However, their roles within the financial ecosystem remain distinct. Tether (USDT) retains dominance in high-frequency crypto trading and emerging market fiat arbitrage, while USDC has consolidated its position as the preferred vehicle for regulated institutional flows and on-chain settlement.

The divergence in market share reflects a broader institutional preference for compliance and transparency. While USDT benefits from network effects and legacy liquidity in decentralized exchanges, USDC’s growth is driven by its alignment with U.S. regulatory standards and its integration into traditional finance infrastructure. This split is evident when comparing their primary use cases and reserve structures.

The following comparison outlines the structural differences between the two dominant issuers:

| Metric | USDT | USDC |

|---|---|---|

| Market Dominance | Highest volume; primary trading pair | Second largest; growing institutional share |

| Primary Use Case | Crypto trading, emerging market remittances | Institutional settlement, regulated DeFi |

| Regulatory Profile | Offshore entity; periodic reserve attestations | U.S. based; monthly attestations, bank partners |

| Reserve Composition | Cash, short-term Treasuries, commercial paper | Cash and short-term U.S. Treasuries |

| Flow Velocity | High; rapid rotation between exchanges | Lower; longer holding periods for treasury yield |

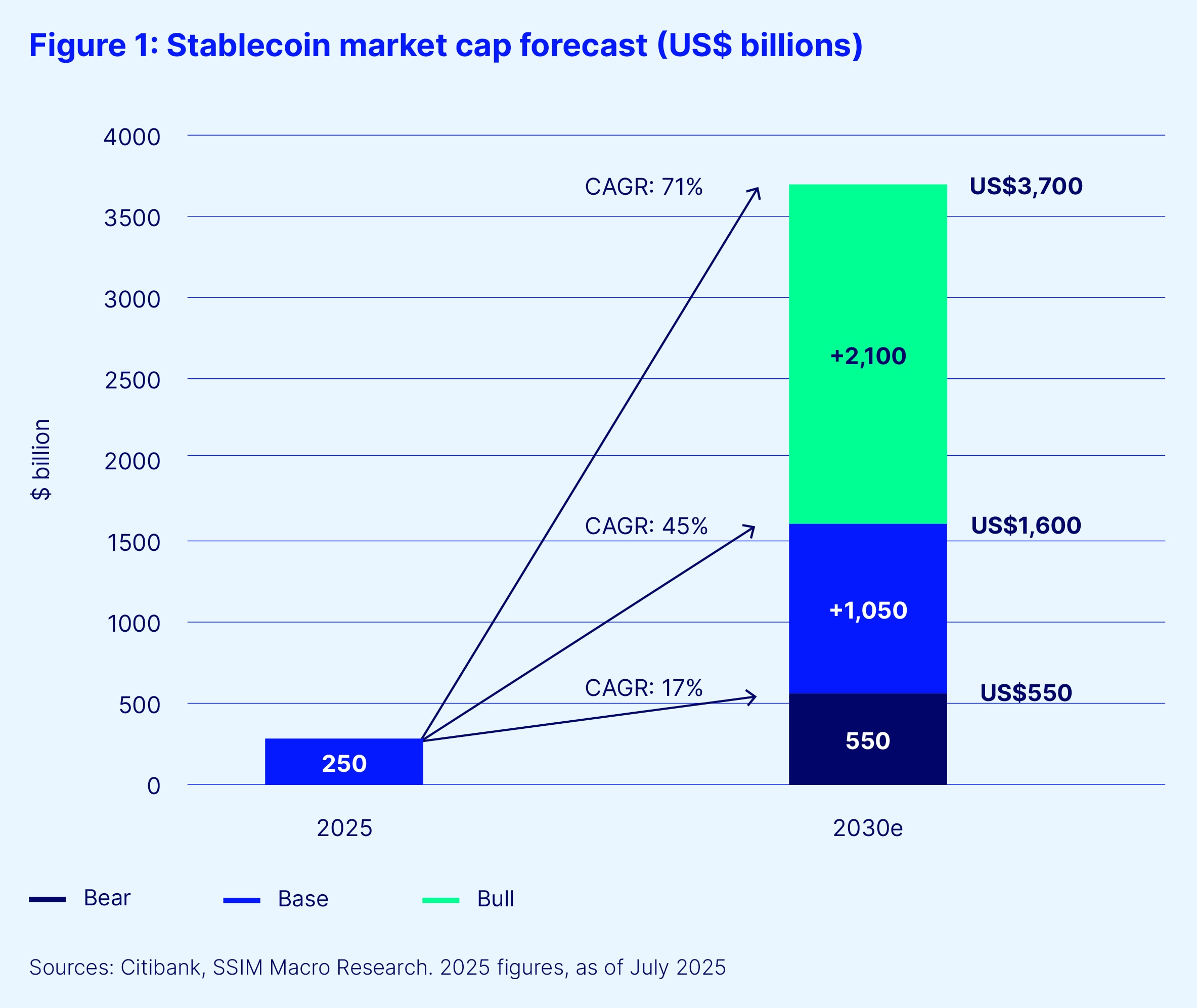

RWA tokenization driving institutional demand

Real-world asset (RWA) tokenization is transforming stablecoins from mere payment rails into foundational settlement infrastructure. By tokenizing treasury bills, private credit, and real estate, institutions are creating a sticky, yield-bearing layer of demand that extends far beyond simple transactional needs. This shift anchors stablecoin utility in the traditional financial system, ensuring that USDC and USDT remain integral to capital markets rather than peripheral crypto assets.

The mechanism is straightforward: institutions hold stablecoins to settle tokenized assets instantly, 24/7, without the friction of traditional clearinghouses. This creates a structural floor for demand. As Deutsche Bank notes in its 2026 digital assets outlook, the rise of stablecoins is now deeply intertwined with the digitization of traditional securities, moving beyond speculative trading into core treasury management [[src-serp-1]].

Regulatory clarity is accelerating this adoption. New global frameworks are reshaping how stablecoins interact with traditional debt, particularly US Treasuries. As the Payments Association highlights, these rules are not just compliance hurdles; they are accelerating adoption by legitimizing stablecoins as a primary vehicle for holding short-term US debt on-chain [[src-serp-5]]. This regulatory tailwind makes USDC and USDT the preferred settlement tokens for institutional RWA platforms.

The result is a new market dynamic where stablecoin supply grows in lockstep with traditional asset tokenization. This is not speculative volume; it is institutional balance sheet expansion. As tokenization matures, the demand for stablecoins will be driven by the need for efficient, compliant settlement of real-world value, securing their long-term relevance in global finance.

Cross-border payments and regulatory shifts

New global regulations are fundamentally altering how institutions treat stablecoin flows. The European Union’s Markets in Crypto-Assets (MiCA) regulation and ongoing legislative efforts in the United States are moving digital assets from a gray area into a regulated financial infrastructure. This shift is not merely about compliance; it is about standardization. For enterprises, the clarity provided by frameworks like MiCA reduces legal uncertainty, making stablecoins a viable tool for treasury management and cross-border settlements rather than just a speculative asset.

The result is a convergence of traditional finance standards with blockchain efficiency. Institutions are no longer treating stablecoin transfers as informal transactions. Instead, they are applying the same rigorous controls used in foreign exchange and wire transfers. As noted by Stripe, stablecoin flows must be treated with the same sensitivity as any other financial process, requiring verification, multisig approvals, and continuous wallet monitoring. This institutionalization ensures that the speed advantage of blockchain is not undermined by operational risk.

Thunes highlights that 2026 marks the year stablecoins become a practical, regulated tool for moving liquidity across borders. The combination of faster settlement and tighter regulatory oversight is reshaping demand for US debt instruments tied to stablecoin reserves. The UK is also finalizing its own framework to keep pace, signaling a global trend toward harmonized rules. This regulatory clarity is accelerating adoption among banks and payment providers who previously hesitated due to compliance fears.

For institutional players, the message is clear: stability comes from regulation. The market is consolidating around compliant issuers like USDC and USDT, which have the legal standing to operate in major jurisdictions. This standardization makes stablecoins safer for enterprise use, bridging the gap between the speed of crypto and the security requirements of traditional banking.

Key Questions on Stablecoin Adoption

Tether (USDT) remains the largest stablecoin issuer by global volume and market share. It is important to distinguish between the issuer and the holders; while Tether issues the asset, the largest holders are typically institutional traders and exchanges utilizing USDT for liquidity and settlement. The total stablecoin supply held steady near $270 billion as of January 2026, with USDT continuing to dominate this landscape [src-serp-8].

No comments yet. Be the first to share your thoughts!