Institutional capital drives stablecoin flows in 2026

Stablecoin flows in 2026 are no longer defined by retail speculation but by institutional adoption. This shift marks a structural change in how digital capital moves, with stablecoins transitioning from experimental assets to core financial infrastructure. The data confirms that momentum is now driven by high-value financial flows rather than small-scale trading activity.

The scale of this institutional entry is evident in transaction volume growth. According to the ZeroHash Stablecoin Momentum Report, active stablecoin usage on their platform grew 146% year over year, while transaction volume surged by 690%. This disparity between user growth and volume growth signals that fewer, larger entities are moving significant capital through stablecoin rails.

This trend is further supported by broader market data. The BVNK Stablecoin Utility Report 2026 notes that half of stablecoin holders have increased their holdings in the last 12 months, with 56% planning to acquire more. These figures suggest a deepening commitment from institutional players who view stablecoins as a primary vehicle for liquidity management rather than a speculative tool.

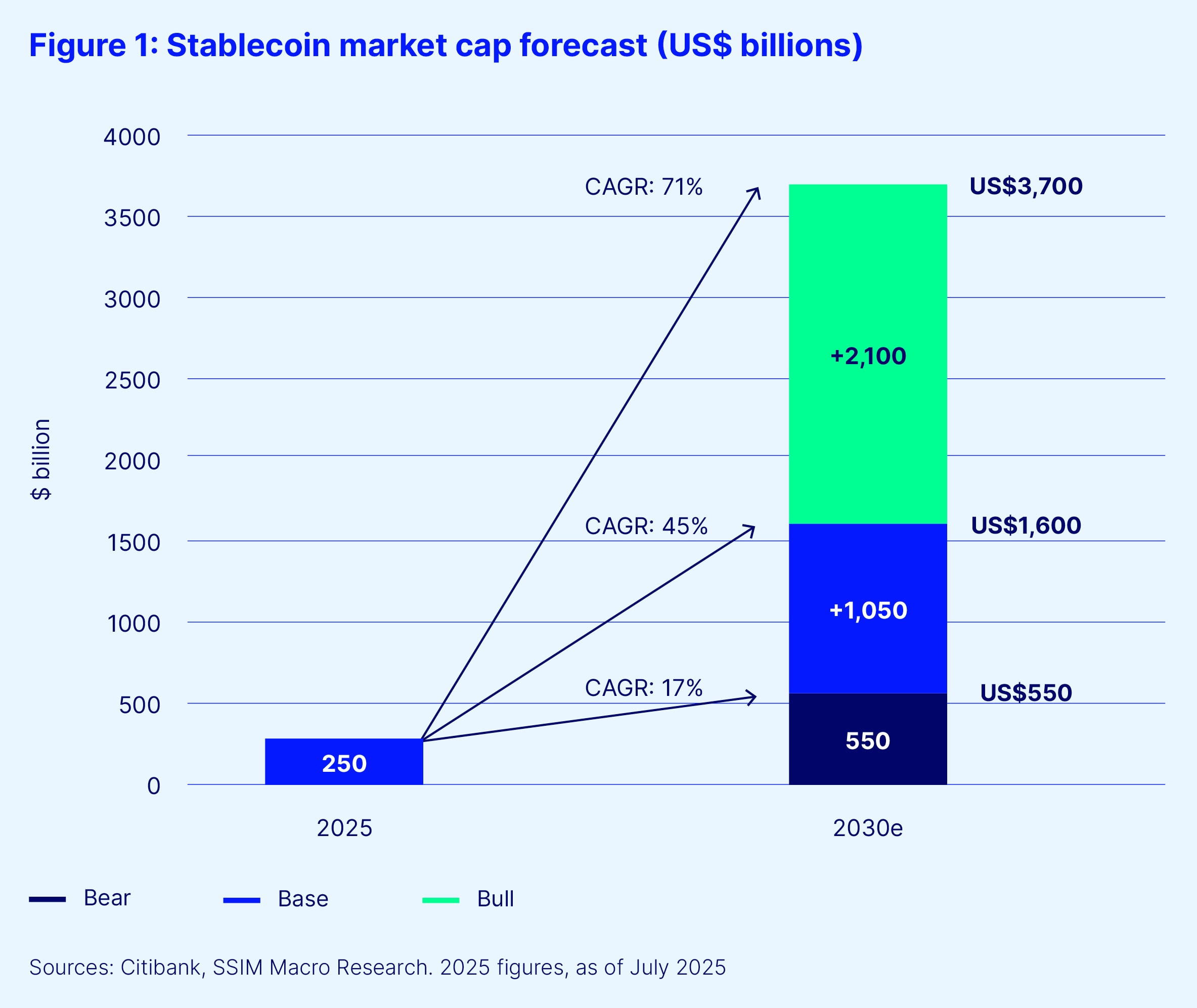

To visualize the magnitude of this inflow, the following chart tracks stablecoin market capitalization over the last 12 months. The steady upward trajectory reflects the consistent accumulation of capital by institutional entities seeking efficiency in cross-border settlements and treasury management.

USDC vs USDT dominance in institutional flows

The 2026 stablecoin landscape is defined by a clear divergence in use cases. While USDT (Tether) retains dominance in retail trading volume and speculative crypto markets, USDC (USD Coin) has become the preferred vehicle for institutional flows. This split is driven primarily by regulatory clarity, transparency requirements, and the structural trust institutions demand when moving large sums of capital.

New global stablecoin rules are accelerating this shift, shaping demand for US debt and pressuring jurisdictions to finalize frameworks that favor regulated issuers. For institutions, the choice is no longer just about liquidity depth; it is about compliance and auditability. USDC’s regulatory alignment makes it the safer choice for corporate treasuries, payment processors, and traditional finance (TradFi) integrations, while USDT remains the backbone of decentralized finance (DeFi) trading pairs where anonymity and speed often outweigh regulatory concerns.

The following comparison highlights the key differences driving this institutional preference.

| Feature | USDC | USDT |

|---|---|---|

| Regulatory Status | Fully regulated, US-based, regular attestations | Offshore, less transparent, ongoing regulatory scrutiny |

| Institutional Adoption | High (corporate treasuries, TradFi integrations) | Low to moderate (primarily crypto-native firms) |

| Transparency | Monthly reserve attestations by Big Four auditors | Quarterly attestations, less detailed reserve breakdown |

| DeFi Liquidity | Strong, but often secondary to USDT in DEXs | Dominant in most DeFi protocols and trading pairs |

| Primary Use Case | Payments, settlement, institutional storage | Speculative trading, cross-border retail transfers |

Cross-border payments reshape global liquidity

Stablecoins have moved past the experimental phase and are now functioning as core financial infrastructure for international settlements. The asset class has crossed a critical threshold, shifting from crypto-native experimentation to a practical tool for moving liquidity across borders faster and under tighter regulatory scrutiny.

This transition is visible in the market data. Stablecoin market capitalization has grown significantly, reflecting increased adoption by institutions seeking efficient cross-border payment rails. The growth trajectory suggests that stablecoins are becoming a standard component of global liquidity management rather than a speculative niche.

Despite this absolute growth, stablecoins still represent only 1% of global payment flows, a share that has remained stubbornly unchanged since 2023. This disparity between explosive absolute growth and static relative share highlights the massive scale of traditional payment networks and the gradual nature of institutional adoption.

The shift toward practice over theory is evident in how financial institutions are integrating these tools. Rather than viewing stablecoins as a temporary crypto trend, banks and payment providers are building permanent infrastructure to leverage their speed and cost advantages for international transfers.

Regulatory frameworks guide institutional adoption

Global regulators are shifting from vague warnings to concrete rulebooks, creating the legal certainty institutional investors require. The European Union’s Markets in Crypto-Assets (MiCA) regulation stands as the first comprehensive framework to legally define "permitted stablecoin issuers." By setting strict reserve requirements and operational standards, MiCA transforms stablecoins from speculative assets into regulated financial instruments, significantly lowering the compliance risk for banks and asset managers entering the space.

In the United States, the regulatory landscape is coalescing around similar principles, though through a patchwork of executive orders and proposed legislation. Agencies are increasingly focusing on the back-end infrastructure—specifically the segregation of customer funds and regular attestation reports—rather than the token itself. This approach mirrors traditional money transmission laws, allowing institutions to integrate stablecoins into existing treasury management systems without building entirely new compliance departments.

The impact is already visible in market data. The rise of regulated issuers is driving liquidity toward US dollar-backed assets, reinforcing their role as the primary bridge between TradFi and DeFi. As Deutsche Bank notes, this focus on stability and legal clarity is accelerating adoption, shaping demand for US debt, and pressuring other jurisdictions, like the UK, to finalize their own frameworks to remain competitive. For institutions, the message is clear: compliance is no longer optional, but the path is now defined.

Key findings from the 2026 stablecoin momentum report

The ZeroHash Stablecoin Momentum Report marks a structural shift in digital asset usage. Stablecoins have crossed a critical threshold, moving from crypto-native experimentation into core financial infrastructure. This transition is defined by two distinct metrics: active usage and transaction volume.

According to the report, active stablecoin usage on ZeroHash grew 146% year over year. More significantly, transaction volume increased 690%. This disparity signals adoption in higher-value financial flows rather than just retail trading. Institutional money is using stablecoins for settlement, liquidity provision, and cross-border payments, driving volume growth far beyond user growth.

The data confirms that stablecoins are no longer a speculative sidecar to the crypto economy. They are becoming a primary rail for value transfer, with institutional actors driving the majority of the volume increase.

No comments yet. Be the first to share your thoughts!