Stablecoin volume and market scale in 2026

The scale of stablecoin activity has shifted from a niche crypto utility to a foundational layer of global digital settlement. By 2026, transaction volumes are accelerating at a pace that outpaces traditional cross-border payment rails, driven by the convergence of regulatory clarity and real-world asset (RWA) tokenization. This growth is not merely speculative; it reflects a structural change in how capital moves across borders and between institutional and retail participants.

Total value locked (TVL) in stablecoin protocols has reached new highs, with USDT and USDC dominating the majority of on-chain settlement. The volume surge is particularly evident in decentralized finance (DeFi) and institutional treasury management, where stablecoins serve as the primary unit of account. This shift is supported by live market data showing sustained upward trends in daily transaction counts and throughput.

The acceleration in volume is largely attributed to the integration of stablecoins into real-world payment systems and the tokenization of traditional assets. As RWAs move on-chain, the demand for fast, low-cost settlement increases, pushing stablecoin usage beyond speculative trading into everyday commerce and institutional finance. This trend is expected to continue as more traditional financial institutions adopt blockchain-based settlement layers.

Regulatory frameworks in major jurisdictions have also played a crucial role in stabilizing the market. Clearer guidelines have encouraged institutional participation, leading to a more mature and resilient stablecoin ecosystem. The result is a market that is less volatile and more integrated with the broader financial system, reflecting the growing importance of stablecoins in the global economy.

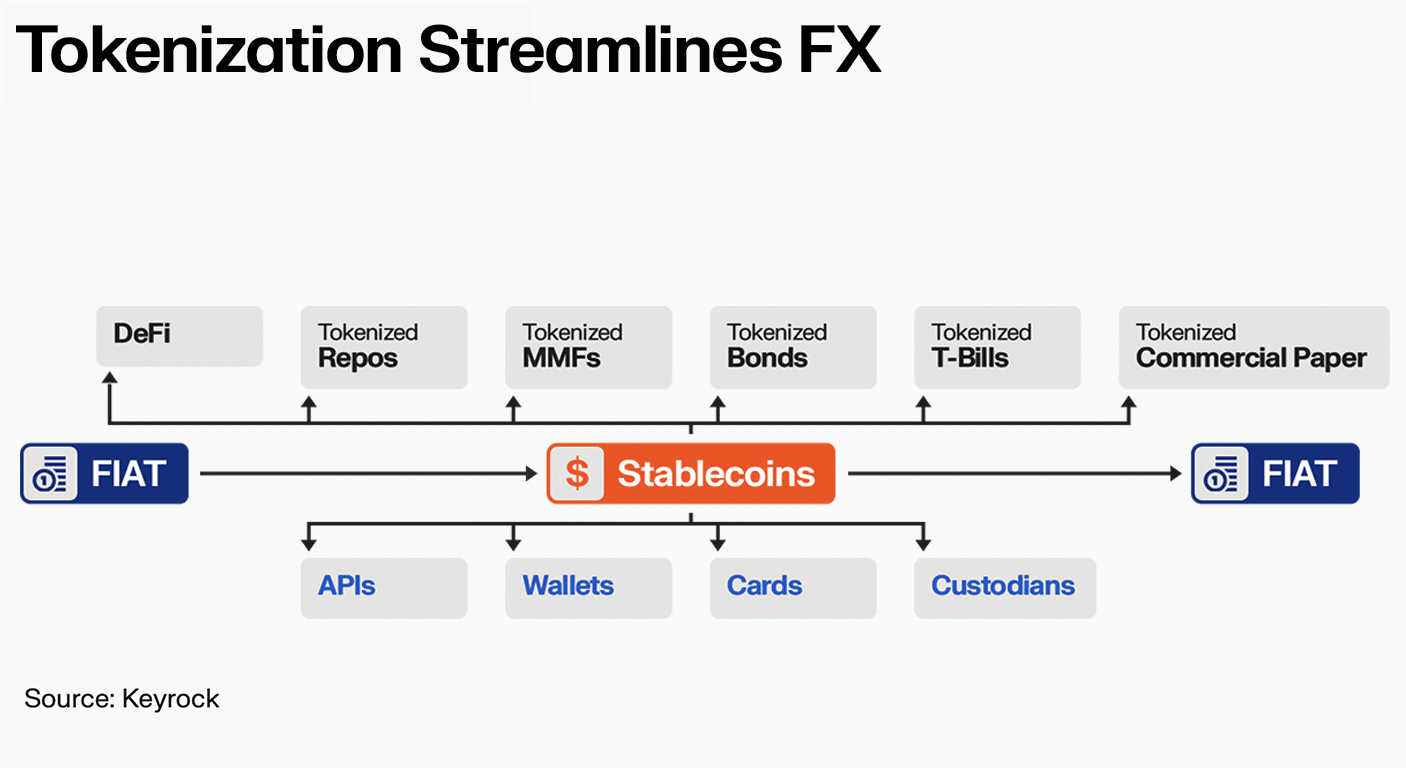

How real-world asset tokenization shifts stablecoin utility

The dominant use case for stablecoins is changing. Historically, the vast majority of stablecoin volume was driven by speculative trading within crypto markets. Deutsche Bank’s 2026 outlook estimates that 85% to 90% of stablecoins were previously used for crypto trading, largely because direct investment in crypto assets remains restricted in many jurisdictions. However, the landscape is shifting as real-world asset (RWA) tokenization matures.

RWA tokenization is moving stablecoins from speculative instruments to essential settlement rails. In 2026, stablecoins are increasingly functioning as payments infrastructure, particularly in business-to-business (B2B) flows and corporate treasury operations. This shift is driven by the need for faster, cheaper cross-border settlements compared to traditional banking systems.

The integration of tokenized assets with stablecoins creates a closed-loop ecosystem. Institutions can hold tokenized treasuries or bonds and settle transactions instantly using stablecoins, reducing counterparty risk and settlement times from days to seconds. This utility expansion is attracting institutional capital that was previously locked out of the crypto ecosystem.

| Feature | Traditional Settlement | RWA + Stablecoin |

|---|---|---|

This structural change is driving record inflows into stablecoins, not as trading collateral, but as operational capital. As regulatory clarity improves, more institutions are adopting this model, further cementing stablecoins as a core component of modern financial infrastructure.

Regulatory frameworks shaping flows

The 2026 regulatory landscape has created a sharp divide in stablecoin utility. Jurisdictions with clear compliance mandates, such as the United States and the European Union under MiCA, have forced issuers to adopt strict reserve and reporting standards. This clarity has attracted institutional capital, turning compliant stablecoins into a preferred vehicle for treasury management and cross-border payments. The European Central Bank and US Treasury guidelines have effectively legitimized these assets for traditional finance integration.

Conversely, regions lacking definitive frameworks have seen liquidity migrate to offshore jurisdictions or decentralized protocols. This regulatory arbitrage has fragmented the market, creating pockets of high-yield but higher-risk liquidity. Issuers operating in gray areas face constant uncertainty, forcing them to either seek regulatory approval or operate in shadows. This split determines where stablecoin capital resides: in regulated on-ramps or in less transparent offshore pools.

The divergence impacts market dynamics significantly. Compliant stablecoins often trade at a premium due to their perceived safety and ease of integration with traditional banking systems. Meanwhile, non-compliant variants may offer higher yields but carry significant counterparty and regulatory risks. As regulations tighten globally, the pressure is mounting for a unified standard, but until then, the flow of capital will continue to follow the path of least regulatory resistance.

The long-term trend points toward greater consolidation among compliant issuers. As regulatory clarity improves, we expect to see a reduction in the number of active stablecoin projects, with the market favoring those that can demonstrate robust compliance and transparent reserves. This shift will likely stabilize the stablecoin market, reducing volatility and increasing trust among institutional investors.

Cross-border payment adoption

Stablecoins have moved from speculative assets to practical infrastructure for moving liquidity across borders. In 2026, businesses are prioritizing speed and lower friction over legacy banking rails, which often involve multi-day settlement times and opaque intermediary fees. This shift is particularly evident in B2B transactions, where predictability and instant finality are critical for cash flow management.

The technical stability of major stablecoins makes them ideal for this use case. Unlike volatile cryptocurrencies, stablecoins maintain a peg to fiat currencies, allowing companies to transact internationally without exposure to sudden price swings. A live view of USDT/USDT shows how these assets remain anchored, providing the reliability needed for high-volume commercial payments.

Adoption is accelerating as regulatory frameworks clarify the rules of engagement. Platforms like Stripe and Thunes are integrating stablecoin capabilities directly into their payment networks, reducing the need for businesses to manage separate crypto wallets or navigate complex compliance hurdles. This integration allows companies to leverage blockchain efficiency while maintaining the familiar interfaces they already use for domestic transactions.

The result is a more efficient global payment ecosystem. Funds that once took three to five business days to clear can now settle in minutes, regardless of the countries involved. This speed reduces working capital requirements and minimizes the risk of errors or lost transfers, making stablecoins a compelling alternative for cross-border trade.

Key questions on 2026 trends

Stablecoin adoption is accelerating as utility expands beyond simple transfers. According to BVNK, half of stablecoin holders increased their holdings in the last 12 months, with 56% planning to acquire more in the near future [src-serp-2]. This growth is driven by six primary forces: regulation, volume, cross-border payments, AI infrastructure, treasury products, and multi-chain architecture [src-serp-2].

What are the stablecoin trends for 2026?

The market is shifting from speculative trading to real-world utility. Regulatory clarity is enabling institutional participation, while cross-border payment solutions are becoming a primary use case for businesses. Additionally, the integration of stablecoins into AI infrastructure and treasury management products is creating new demand vectors that extend beyond traditional retail payments.

How does regulation impact stablecoin flows?

Regulation acts as the primary gatekeeper for institutional capital. Clear frameworks allow banks and asset managers to integrate stablecoins into existing compliance structures. This reduces counterparty risk and encourages the tokenization of real-world assets (RWA), which in turn drives volume on regulated chains.

Are stablecoins replacing traditional treasury instruments?

Not entirely, but they are complementing them. Stablecoins offer 24/7 settlement and programmability that traditional treasury products lack. Companies are using them for liquidity management and cross-border payroll, while keeping larger reserves in traditional instruments for stability.

No comments yet. Be the first to share your thoughts!