Institutional stablecoin adoption accelerates

The stablecoin market has shifted from retail speculation to institutional utility in 2026. This transition is defined by higher transaction values and deeper liquidity pools rather than volume driven by retail trading. Financial institutions are now using stablecoins for settlement, cross-border payments, and treasury management, creating a more stable and predictable flow of capital.

Data from payment infrastructure providers confirms this structural change. ZeroHash reported that active stablecoin usage grew 146% year over year, while transaction volume increased by 690%. These figures signal a move toward higher-value financial flows, where stablecoins serve as a primary settlement layer for business-to-business and institutional transactions.

BVNK’s 2026 Utility Report further validates this trend. The report notes that half of stablecoin holders increased their holdings in the last 12 months, with 56% planning to acquire more. This accumulation pattern reflects institutional confidence in stablecoins as a liquid asset class, rather than a speculative vehicle.

The growth in transaction volume is not merely a function of price appreciation but of actual utility. Institutions are integrating stablecoin rails into their existing financial infrastructure, leveraging the speed and finality of blockchain settlement. This integration is reducing reliance on traditional correspondent banking networks for certain cross-border flows, particularly in emerging markets where liquidity access is critical.

As institutional adoption deepens, the focus shifts from mere adoption metrics to the efficiency of settlement. Stablecoins are becoming a standard component of corporate treasury operations, offering real-time liquidity and reduced friction in international trade. This shift is reshaping the broader financial landscape, with stablecoin flows acting as a key indicator of institutional liquidity preferences.

USDC vs USDT Market Share Dynamics

The stablecoin market is bifurcated by user base and settlement intent. Tether (USDT) retains dominance in global volume and retail circulation, while USD Coin (USDC) captures the institutional segment through regulatory transparency and banking partnerships. This divergence dictates how liquidity flows across cross-border rails and decentralized exchanges.

USDT’s market cap and trading volume remain the highest, driven by its ubiquity in emerging markets and as the primary collateral on many centralized exchanges. Its liquidity depth is unmatched in high-volatility environments, making it the default settlement layer for speculative retail activity. Conversely, USDC’s growth is anchored in B2B payments and institutional custody. Its issuer, Circle, maintains a fully reserve-backed model with regular attestations, aligning with the compliance requirements of traditional finance entities entering the digital asset space.

The choice between these assets is no longer just about price stability; it is a function of regulatory risk and counterparty trust. For institutions managing large-scale treasury operations, USDC’s clear legal structure and US-based regulatory compliance offer a lower risk profile. For retail traders and global remittance users in jurisdictions with less stringent banking infrastructure, USDT’s widespread acceptance and deeper liquidity pools provide superior utility.

The following table compares the core operational differences that drive this market split.

| Feature | USDC | USDT |

|---|---|---|

| Primary Issuer | Circle (US-based) | Tether (Offshore) |

| Regulatory Stance | High compliance, US-regulated | Lower transparency, offshore |

| Primary Use Case | Institutional B2B, Treasury | Retail trading, Global remittance |

| Liquidity Depth | Strong in fiat on-ramps | Deepest across all exchanges |

| Reserve Composition | Cash and short-term Treasuries | Commercial paper, cash, other |

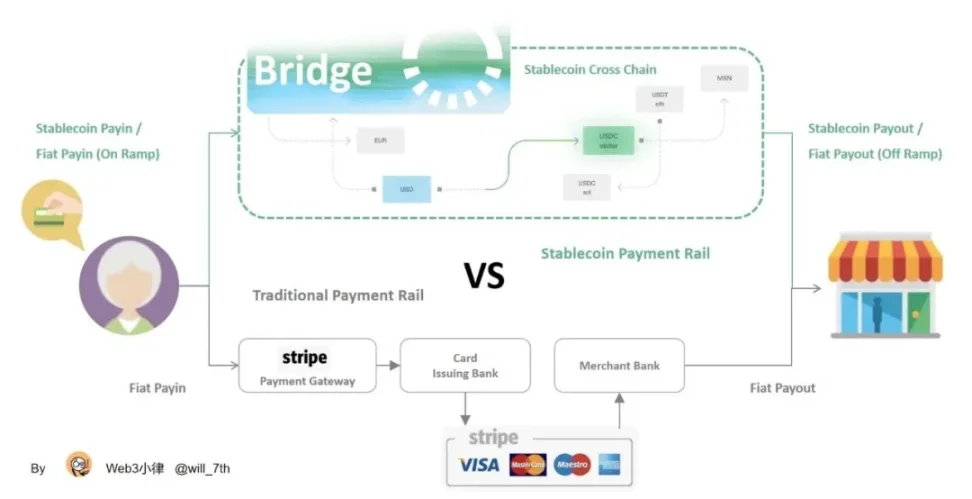

Cross-border payments replace traditional rails

Stablecoins are transitioning from speculative assets to operational infrastructure for B2B cross-border settlements. In 2026, the focus has shifted from theoretical adoption to practical execution, with major payment processors integrating stablecoin rails to reduce friction and cost for international transactions.

While stablecoins remain approximately 1% of global payment flows by value, this share has remained stubbornly unchanged since 2023 despite explosive growth in absolute terms. This stagnation in percentage share masks the rapid expansion of actual transaction volume, as stablecoins capture niche segments where speed and cost efficiency outweigh the inertia of legacy banking systems. The growth is not yet broad enough to disrupt SWIFT’s dominance, but it is significant enough to force traditional players to adapt their liquidity management strategies.

Major financial technology firms are validating this trend through direct integration. Stripe, BVNK, and Thunes have all expanded their stablecoin capabilities in 2026, providing the regulatory and technical infrastructure necessary for institutional adoption. These platforms allow businesses to settle payments in stablecoins while managing fiat on-ramps and off-ramps seamlessly, effectively bridging the gap between traditional banking and blockchain liquidity.

For corporate treasurers, this shift offers a tangible alternative to the 2-3 day settlement times and high fees associated with correspondent banking. By leveraging stablecoin rails, businesses can achieve near-instant settlement across multiple jurisdictions, reducing the need for pre-funded nostro accounts and freeing up working capital. This efficiency gain is particularly valuable for high-volume, low-margin transactions where traditional banking costs erode profitability.

Real-world asset tokenization trends

Institutional liquidity is increasingly flowing into tokenized real-world assets (RWA), creating a direct bridge between traditional finance and blockchain-based settlement. This shift is not merely speculative; it represents a structural change in how value is stored and transferred. As noted by Stripe, large-scale stablecoin adoption could eventually shift deposits away from traditional banks, concentrating reserves within a few key financial institutions. This consolidation highlights the growing importance of stablecoins as the primary settlement layer for institutional capital.

The integration of RWA into stablecoin ecosystems allows for greater liquidity efficiency. By tokenizing assets such as treasury bills or private credit, institutions can access 24/7 markets without the friction of legacy clearinghouses. BVNK and Thunes have highlighted how this infrastructure supports faster cross-border settlements, reducing the time capital is tied up in transit. For businesses, this means working capital is no longer locked in multi-day processing windows.

As stablecoins evolve from niche crypto instruments to core payments infrastructure, their role in B2B flows and treasury operations becomes critical. The 2026 landscape suggests that stablecoins will function as the plumbing for global finance, enabling seamless integration between tokenized assets and traditional banking rails. This convergence reduces counterparty risk and enhances transparency, making tokenized RWA a standard component of institutional liquidity management.

Regulatory frameworks reshape liquidity

Global regulatory structures are moving from experimental guidelines to enforceable mandates, directly impacting how institutional capital flows through stablecoin rails. The implementation of the Markets in Crypto-Assets (MiCA) regulation in the European Union and evolving frameworks in the United States are creating a standardized environment for liquidity providers. This standardization reduces legal ambiguity, allowing institutions to integrate stablecoins into existing treasury and settlement operations with greater confidence.

Regulatory clarity acts as a filter for market participants. Institutions are increasingly prioritizing stablecoins that comply with strict reserve auditing and issuance transparency requirements. This shift is evident in the growing preference for US dollar-pegged assets that meet official compliance standards, as opposed to algorithmic or lightly regulated alternatives. The resulting liquidity pools are deeper and more resilient, characterized by lower slippage during high-volume settlement periods.

Payment processors are adapting their infrastructure to align with these new rules. Stripe, BVNK, and Thunes have updated their compliance protocols to support regulated stablecoin transactions, signaling that the technology is now considered mature for enterprise use. These platforms facilitate the movement of value across borders while ensuring that the underlying liquidity adheres to jurisdictional requirements. This integration ensures that stablecoin flows do not bypass traditional banking oversight but rather operate within it.

The convergence of regulatory compliance and technological infrastructure is stabilizing the stablecoin market. By enforcing clear rules on reserves and issuance, regulators are effectively institutionalizing the asset class. This process transforms stablecoins from speculative instruments into reliable tools for global liquidity management and cross-border settlement.

No comments yet. Be the first to share your thoughts!