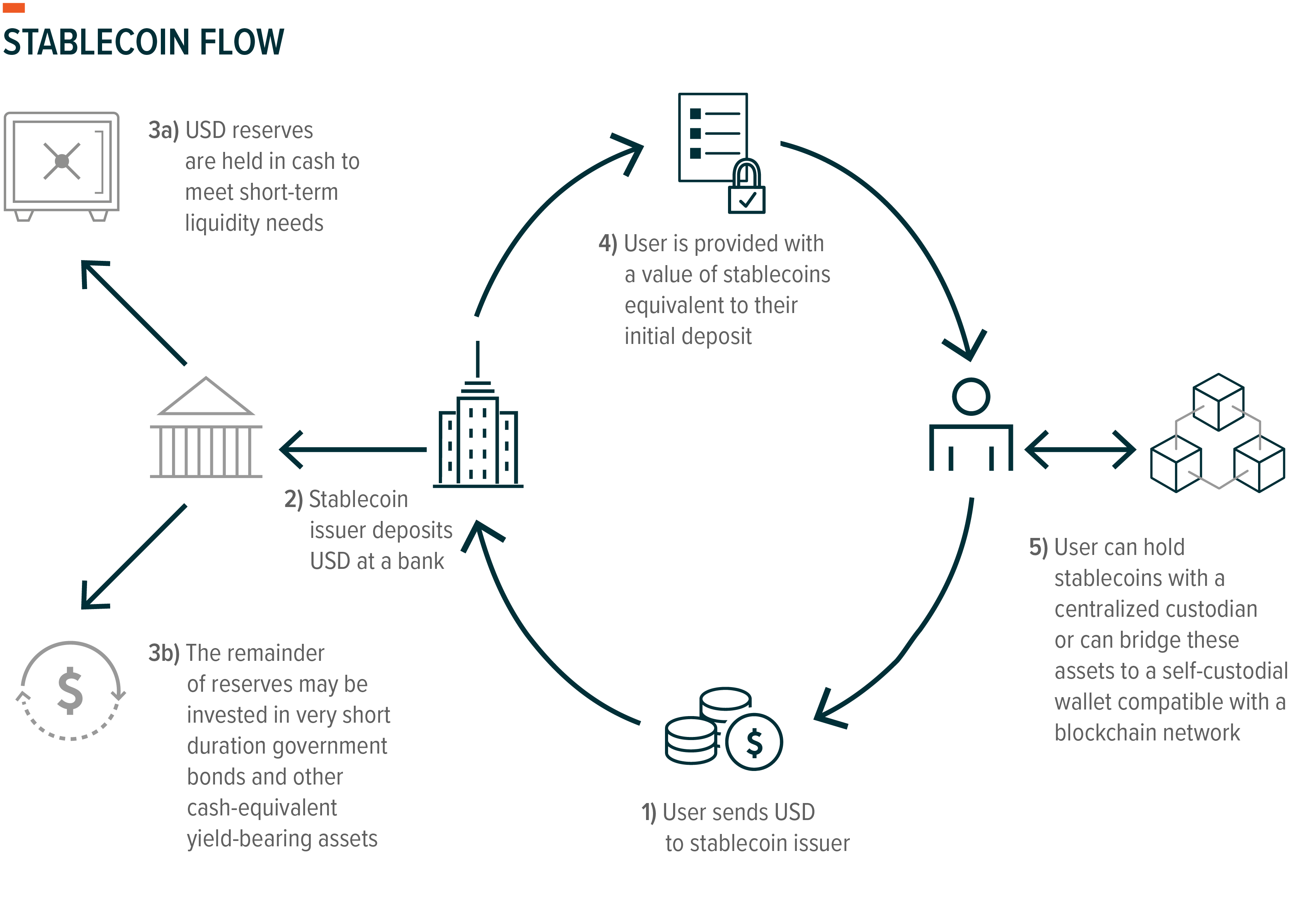

Stablecoin flows in 2026

Stablecoin flows in 2026 have shifted from speculative trading volume to functional payments infrastructure. The dominant narrative is no longer about price appreciation, but about utility. Cross-border transfers, remittances, B2B settlements, and treasury operations increasingly run through stablecoin rails because the efficiency gains are immediate and measurable.

This shift is most visible in the inflow of institutional capital into regulated assets like USDC and EURC. RWA tokenization has acted as the primary driver, bridging traditional finance with on-chain liquidity. As Fidelity launched its own USD-pegged stablecoin (FIDDSM) in early 2026, the market confirmed that legacy financial institutions are building their own rails rather than relying solely on third-party issuers.

The result is a more fragmented but robust ecosystem. Capital flows are no longer just about arbitrage; they are about settlement speed and regulatory compliance. For institutional investors, this means stablecoins are becoming a standard tool for moving liquidity across borders, faster and under tighter regulatory frameworks than traditional banking allows.

Evaluating Stablecoin Flow Tradeoffs in 2026

As stablecoins transition from speculative assets to essential payments infrastructure, the decision to move capital into USDC, EURC, or emerging issuers like Fidelity’s FIDDSM requires a rigorous evaluation of tradeoffs. In 2026, the focus has shifted from yield-chasing to operational reliability, regulatory compliance, and cross-border efficiency. Readers must weigh the benefits of deep liquidity against the specific risks of issuer concentration and jurisdictional exposure.

Liquidity and Settlement Speed

The primary driver for institutional adoption is the ability to settle value instantly across borders without traditional banking delays. USDC and EURC benefit from entrenched liquidity pools on major decentralized and centralized exchanges, ensuring that large institutional flows can execute with minimal slippage. However, speed alone does not guarantee efficiency; it must be paired with predictable finality. When evaluating flow tradeoffs, consider that some newer stablecoins may offer faster settlement on niche chains but lack the depth to handle multi-million dollar treasury operations without significant price impact.

Regulatory Clarity and Custody

Regulatory certainty is the most critical differentiator in 2026. Issuers operating under clear frameworks, such as Fidelity’s FIDDSM which is fully collateralized with cash and US Treasuries, provide a layer of trust that reduces counterparty risk for institutional treasuries. In contrast, stablecoins with opaque reserve structures or those operating in regulatory gray zones pose significant compliance headaches. Institutions must verify that their stablecoin holdings are subject to regular, audited attestations and that the issuer maintains robust multisig approval processes and wallet monitoring systems to prevent unauthorized outflows.

Currency Exposure and Hedging

The choice between USD-pegged and EUR-pegged stablecoins often comes down to natural hedging needs. EURC provides a direct solution for European entities seeking to settle invoices in euros without converting to USD first, thereby eliminating foreign exchange friction. However, this benefit is offset by the liquidity depth of USD-based assets. For global businesses, holding a diversified basket of stablecoins may be necessary, but it introduces complexity in accounting and reserve management. The tradeoff lies between the operational simplicity of a single dominant currency and the hedging benefits of a multi-currency approach.

Cost Structure and Hidden Fees

While on-chain transfers are often cheaper than traditional wire transfers, the total cost of ownership includes gas fees, exchange spreads, and custody fees. High-frequency treasury operations can see these costs accumulate rapidly. Institutions should compare the all-in cost of moving funds via USDC on Ethereum mainnet versus layer-2 solutions or alternative chains. The tradeoff here is between security and cost; mainnet Ethereum offers the highest security but at a premium, while cheaper alternatives may expose the institution to greater smart contract risk or lower liquidity during peak volatility.

| Evaluation Factor | Primary Strength | Primary Weakness | Best Use Case |

|---|---|---|---|

| Liquidity Depth | High slippage resistance for large trades | Can be chain-dependent | High-volume B2B settlements |

| Regulatory Status | Clear compliance framework (e.g. FIDDSM) | Higher barrier to entry for smaller issuers | Institutional treasury compliance |

| Currency Match | Eliminates FX conversion fees | Limited to specific regional markets | Regional invoice payments |

| Settlement Speed | Near-instant finality | Variable gas costs on mainnets | Time-sensitive cross-border transfers |

Operational Verification

Finally, the operational integrity of stablecoin flows must be treated with the same rigor as traditional financial processes. This means implementing verification steps, multisig approvals, and continuous audit trails for every transaction. The tradeoff between ease of use and security is stark; automated, single-signature flows are faster but riskier. Institutions must decide whether the speed of automated treasury management justifies the exposure to potential smart contract vulnerabilities or unauthorized access. In 2026, the most successful adopters are those that balance this tension by embedding security checks directly into their workflow rather than treating them as afterthoughts.

How to Choose the Next Step for RWA and Stablecoin Capital

Institutional capital is no longer just watching stablecoins; it is routing them. The 2026 market has shifted from speculative trading to utility, with USDC and EURC serving as the primary rails for tokenized real-world assets (RWA). For treasury teams and asset managers, the decision is no longer whether to adopt stablecoin infrastructure, but how to structure it for compliance and efficiency.

Use this framework to evaluate your next move. Each step addresses a specific operational or regulatory checkpoint required for institutional-grade stablecoin deployment.

Before selecting a token, quantify where cash is stuck. Traditional wire transfers and ACH networks introduce latency and hidden fees that erode margin on B2B settlements and cross-border remittances. Identify transaction volumes where same-day settlement is currently impossible or prohibitively expensive. Stablecoins like USDC provide a 24/7 rail that cuts settlement times from days to minutes, directly improving working capital velocity.

Institutional adoption hinges on trust and legal clarity. Ensure your chosen stablecoin issuer maintains full reserves in cash and short-dated US Treasuries, as required by emerging US and EU regulations. For custody, avoid personal wallets; instead, engage licensed digital asset custodians or bank-affiliated services that offer insurance and audit trails. New entrants like Fidelity’s FIDDSM illustrate how traditional finance giants are backing stablecoins with full-service compliance models, offering a familiar risk profile for conservative institutional investors.

Match the stablecoin to your operational geography. USDC is the dominant choice for USD-denominated RWA tokenization and US-based treasury operations, benefiting from strong US regulatory clarity. If your institution operates heavily in Europe or handles EUR-denominated settlements, EURC provides a direct Euro peg with similar transparency. Using the correct currency rail eliminates foreign exchange friction and reduces the complexity of multi-currency treasury management.

Stablecoins are not a standalone product; they are an infrastructure layer. Integrate stablecoin wallets and transaction monitoring directly into your Treasury Management System or Enterprise Resource Planning (ERP) software. This integration allows your finance team to view crypto holdings alongside traditional cash balances, ensuring accurate reporting and automated reconciliation. Without this technical bridge, stablecoin operations will remain siloed and difficult to audit.

Avoid the weak options

Use this section to make the Stablecoin Flow Report decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Stablecoin flows 2026: what to check next

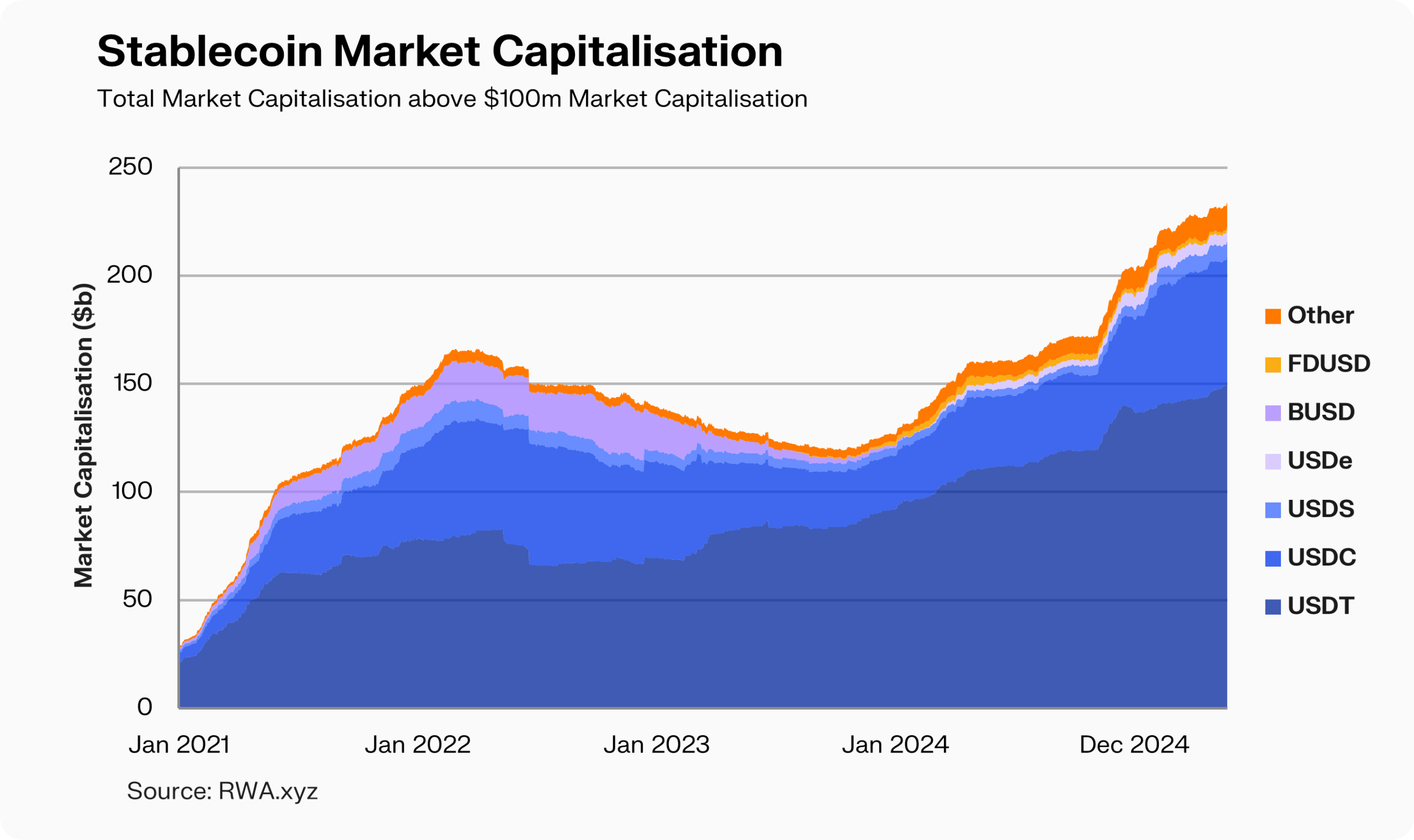

Stablecoins have shifted from speculative assets to operational infrastructure. In 2026, the primary use case is moving liquidity across borders for B2B settlements and treasury management. While absolute volumes are growing, stablecoins still represent roughly 1% of global payment flows, a share that has remained stubbornly flat since 2023 despite explosive nominal growth.

Institutional adoption is accelerating, driven by tighter global regulations and the emergence of fully collateralized products. Fidelity Digital Assets recently launched FIDDSM, a stablecoin pegged 1:1 to the US dollar and backed by cash and US Treasurys. This move signals a broader trend where traditional finance providers are entering the space with strict compliance models.

No comments yet. Be the first to share your thoughts!