Institutional inflows reshape stablecoin markets

The stablecoin landscape in 2026 has shifted decisively from retail speculation to institutional utility. This transition is no longer theoretical; it is driven by concrete regulatory frameworks and the practical demands of global commerce. The passage of the GENIUS Act in the United States has established a clear regulatory baseline for stablecoins, transforming them from ambiguous digital assets into compliant financial instruments. This legal clarity has enabled large-scale capital to enter the market with confidence, prioritizing regulated stablecoins that offer transparent reserves and auditability.

Institutional actors are now leveraging stablecoins for cross-border payments and treasury management, bypassing the inefficiencies of traditional banking rails. According to analysis by Forbes, 2026 has seen considerable discussion around stablecoins, albeit with an increasing focus on action compared to 2025. Major payment processors and financial institutions are integrating stablecoin infrastructure to facilitate faster, cheaper settlements. This shift reflects a broader trend where stablecoins are viewed as essential liquidity tools rather than speculative vehicles.

The rise of institutional inflows has also impacted market dynamics, with regulated stablecoins capturing a larger share of total volume. Data from Stripe and BVNK indicates that business-to-business (B2B) payments are increasingly settled in stablecoins, particularly for international trade. This demand is supported by the growing adoption of tokenized assets in traditional finance, further blurring the lines between crypto and conventional markets.

To understand the financial implications of this shift, financial professionals can use the calculator below to estimate potential cost savings from using regulated stablecoins for cross-border transactions compared to traditional wire transfers. The model assumes a standard transaction size and compares fees, settlement times, and foreign exchange spreads.

USDC and USDT Liquidity Pool Comparison

Institutional treasury management and DeFi liquidity provision require distinct operational profiles. While both USDC and USDT maintain peg stability, their structural differences dictate specific use cases. USDC aligns with regulated treasury functions due to its transparent reserve composition and compliance frameworks. USDT dominates global exchange liquidity and cross-border settlement volumes, offering deeper order books but with varying transparency standards.

The following comparison outlines the divergent characteristics of these assets. Understanding these distinctions is essential for legal and compliance teams evaluating counterparty risk and regulatory exposure in 2026.

The choice between these stablecoins often hinges on the trade-off between regulatory certainty and liquidity depth. For entities operating under strict jurisdictional oversight, USDC provides a more defensible compliance posture. Conversely, for operations requiring rapid global settlement through the deepest available markets, USDT remains the dominant vehicle. Treasury policies should explicitly define acceptable stablecoin ratios based on these operational requirements.

Calculate cross-border payment costs

Determining the true cost of cross-border transactions requires comparing the fee structures of legacy correspondent banking against stablecoin networks. Traditional fiat rails typically charge a flat fee plus a percentage of the transaction value, often compounded by foreign exchange spreads. In contrast, stablecoin transactions are governed by network gas fees and minimal exchange spreads, resulting in significantly lower overhead for high-volume institutional flows.

The following calculator quantifies these differences. Input the transaction amount and destination region to observe the cost disparity between SWIFT-based transfers and stablecoin settlements.

Step 1: Define the transaction parameters

The calculation begins by establishing the principal amount and the destination jurisdiction. The financial impact of fixed fees diminishes as transaction volumes increase, making the percentage-based components of traditional banking fees the primary driver of cost inefficiency for large institutional transfers.

Input the exact USD value of the cross-border payment. This figure serves as the baseline for calculating both the fixed network fees and the percentage-based spreads applied by traditional banking intermediaries.

Step 2: Select the destination region

Geographic destination significantly influences the final cost due to varying correspondent banking relationships and regulatory compliance requirements. Regions with less developed banking infrastructure often incur higher spreads and additional intermediary fees when using traditional rails.

Choose the target jurisdiction from the dropdown menu. The calculator adjusts the estimated gas fees and traditional banking spreads based on historical data for this specific region, reflecting the complexity of local compliance and liquidity availability.

Step 3: Analyze the cost differential

The output provides a direct comparison of total costs. Traditional SWIFT transfers include a base fee, a percentage-based intermediary fee, and a foreign exchange spread. Stablecoin costs are primarily driven by network gas fees and a minimal exchange spread, offering greater predictability and transparency for financial professionals.

Compare the calculated totals. The stablecoin cost reflects the actual on-chain transaction fee plus a negligible spread, while the traditional cost includes hidden FX markups and multiple intermediary charges. This differential highlights the operational savings available through institutional stablecoin adoption.

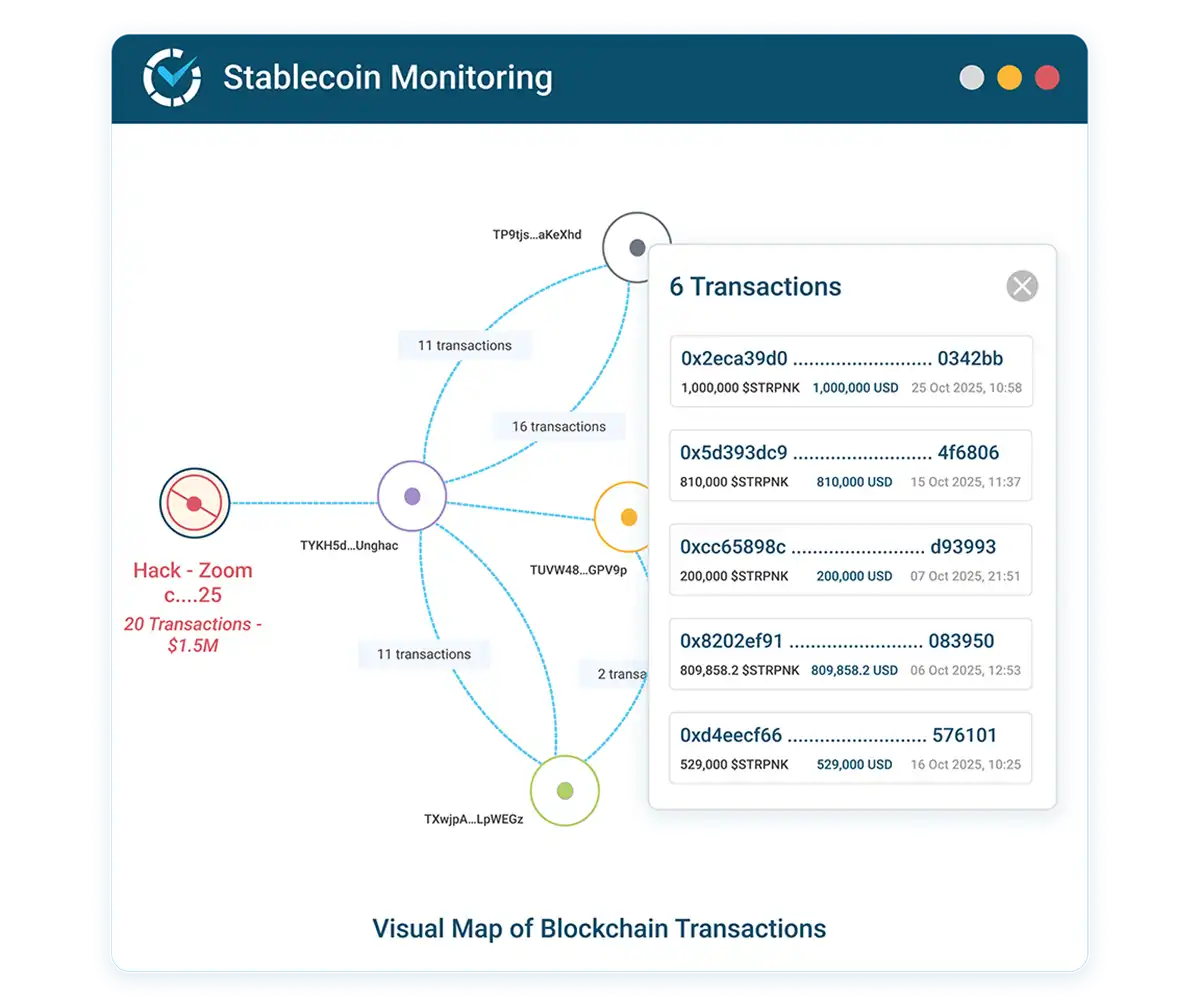

Assess regulatory compliance requirements

Institutions must treat stablecoin flows as sensitive financial processes requiring strict verification and monitoring. The regulatory landscape is shifting rapidly, with new global rules accelerating adoption while pressuring jurisdictions like the UK to finalize their own frameworks. To navigate this environment, legal and operational safeguards must be embedded directly into the transaction workflow.

Compliance begins with robust internal controls. Stripe notes that businesses should implement multisig approvals, comprehensive audit trails, and continuous wallet monitoring to mitigate risk. These measures ensure that every transfer is authorized by multiple parties and fully traceable, satisfying both internal governance standards and external regulatory expectations.

The following calculator helps finance teams estimate the potential cost of compliance overhead relative to transaction volume. This estimate includes baseline audit fees and monitoring infrastructure costs, allowing institutions to factor these into their operational budgets.

The formula applies a fixed audit fee per transaction ($15) plus a variable monitoring cost (0.05% of volume). This structure reflects current industry standards for maintaining secure, compliant stablecoin operations at scale.

Stablecoin Selection Framework

Selecting a stablecoin in 2026 requires aligning asset choice with specific regulatory and liquidity requirements. Institutional capital allocation depends on reserve transparency, exchange depth, and compliance with evolving financial frameworks. The following analysis addresses common inquiries regarding stablecoin utility and selection criteria.

No comments yet. Be the first to share your thoughts!