Regulatory clarity drives institutional adoption

The passage of the GENIUS Act in the United States established the first comprehensive federal regulatory framework for stablecoins, shifting the narrative from speculative uncertainty to structured compliance. This legislative milestone reclassified stablecoins as regulated treasury instruments, allowing institutional investors to integrate them into balance sheets with the same rigor applied to traditional money market funds.

Prior to 2026, the absence of clear federal guidelines forced many large financial institutions to treat stablecoins as high-risk liabilities. The new framework mandates reserve transparency, regular audits, and strict capital requirements, effectively neutralizing the counterparty risks that previously deterred corporate treasurers. As a result, stablecoins are no longer viewed merely as trading pairs but as efficient vehicles for cross-border settlements and yield generation.

Global regulatory bodies are now aligning their policies with this new US standard. The Payments Association notes that these new global rules are accelerating adoption and shaping demand for US debt, as stablecoin reserves increasingly back treasuries. This shift is pressuring other jurisdictions, such as the UK, to finalize their own frameworks to remain competitive. The result is a more unified global financial landscape where digital dollars operate with the predictability of traditional banking rails.

Cross-border payments replace speculative trading

The dominant narrative around stablecoins in 2026 has shifted from retail speculation to institutional utility, with cross-border B2B payments emerging as the primary use case. While stablecoins still represent a small fraction of total global payment volume, their adoption in treasury operations reflects a pragmatic response to the inefficiencies inherent in legacy correspondent banking. This transition marks a move from theoretical potential to practical application, driven by the need for speed, transparency, and cost reduction in international settlements.

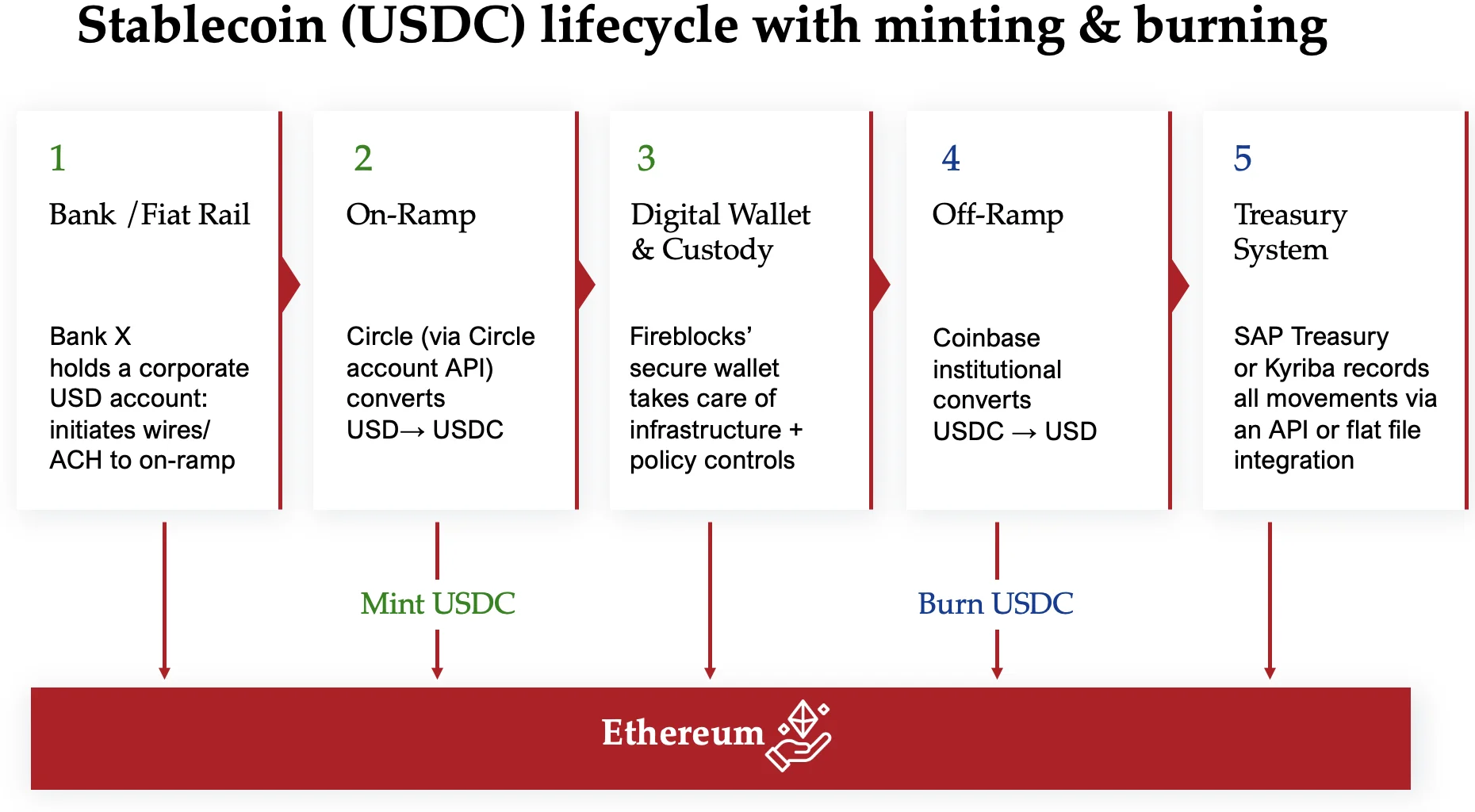

Traditional SWIFT rails remain the backbone of global finance but are increasingly viewed as archaic for high-frequency treasury operations. SWIFT transactions often take one to five days to settle, involve multiple intermediary banks that each take a fee, and lack real-time visibility into funds in transit. In contrast, stablecoin transfers settle in minutes or seconds, 24/7, with significantly lower transaction costs. For multinational corporations managing liquidity across diverse jurisdictions, this efficiency translates directly into improved working capital management and reduced foreign exchange risk.

Regulatory clarity has further accelerated this shift. With frameworks like the EU’s MiCA and evolving guidelines from US regulators, institutions are now more confident in deploying stablecoins for operational payments rather than mere trading. Companies are leveraging regulated stablecoins like USDC, which is backed by cash and short-dated US treasuries, to move liquidity across borders without exposing funds to the volatility associated with Bitcoin or Ethereum. This regulatory tailwind has enabled fintechs and traditional banks to build infrastructure that bridges fiat and digital assets seamlessly.

The integration of stablecoins into treasury strategies is not about replacing traditional banking entirely but about optimizing specific pain points. For instance, payroll processing for international contractors, supplier payments in emerging markets, and intercompany fund transfers are areas where stablecoins offer immediate value. By reducing the friction and cost of moving money globally, stablecoins are becoming a critical component of modern treasury infrastructure, complementing rather than competing with traditional financial systems.

The data supports this operational focus. While speculative trading volumes remain high, the growth in stablecoin supply is increasingly correlated with actual payment activity. Institutions are holding stablecoins as cash equivalents for immediate liquidity needs, rather than as speculative assets. This behavioral shift is evident in the rising number of institutional wallets and the increasing volume of stablecoins held by regulated custodians. The trend indicates a maturing market where utility drives demand, not just speculation.

For legal and compliance teams, this shift requires a new approach to risk management. Understanding the regulatory status of the stablecoin issuer, the jurisdiction of the recipients, and the anti-money laundering (AML) implications of cross-border transfers is essential. The focus is on ensuring that the speed and efficiency of stablecoin payments do not come at the cost of regulatory compliance. As the landscape evolves, institutions that can navigate these complexities will gain a significant competitive advantage in global treasury operations.

Treasury reserves shift to tokenized assets

Corporations are increasingly allocating idle cash into stablecoins, treating them as a functional extension of traditional cash management. This shift effectively creates a new, direct demand for US debt, as most major stablecoins are backed by short-term US Treasury bills. By holding these tokens, corporate treasuries bypass the traditional banking intermediary to gain exposure to sovereign credit, altering the flow of capital in the financial system.

This migration of funds presents a structural change to bank deposit dynamics. As noted by Stripe, large-scale adoption of stablecoins could shift significant deposits away from traditional banks, potentially concentrating reserves in a few key institutions. This dynamic introduces a risk of feedback loops where bank liquidity tightens as deposits migrate to on-chain alternatives, forcing banks to adjust their lending and reserve strategies.

To understand the operational differences, treasurers often compare traditional bank deposits against stablecoin holdings. The following table outlines the key distinctions in yield, speed, and liquidity for 2026.

Key stablecoins for corporate treasuries

Corporate treasuries are increasingly treating stablecoins as a distinct asset class rather than a speculative vehicle. The selection criteria have shifted from yield generation to capital preservation, regulatory clarity, and operational liquidity. In 2026, the institutional landscape is defined by four primary issuers that offer different trade-offs between centralization and decentralization.

USDC: The Regulatory Standard

Circle’s USDC remains the preferred choice for treasuries operating in strict compliance environments. Its reserves are held in short-duration U.S. Treasuries and cash deposits, with regular attestation reports providing transparency. This structure aligns closely with traditional money market fund mechanics, making it easier for finance teams to justify its use in internal audits. USDC’s deep integration with regulated exchanges and banking partners ensures reliable off-ramps to fiat currency.

USDT: The Liquidity Anchor

Tether’s USDT continues to dominate in terms of trading volume and global availability. While its reserve composition has faced historical scrutiny, recent attestations show a significant allocation to commercial paper and other short-term instruments. For treasuries requiring deep liquidity across multiple blockchain networks and exchanges, USDT offers unmatched depth. However, its less transparent reserve structure may present compliance hurdles for institutions subject to strict regulatory oversight.

PYUSD: The Payment Rails Integration

PayPal’s PYUSD offers a unique advantage for companies already embedded in the PayPal ecosystem. As a fully reserved stablecoin issued by Paxos, it provides a seamless bridge between traditional payment processing and blockchain settlements. This integration is particularly valuable for cross-border payments and e-commerce settlements, reducing friction in customer-facing transactions. Its regulatory compliance with New York State banking authorities adds a layer of trust for conservative treasuries.

DAI: The On-Chain Alternative

MakerDAO’s DAI represents the primary decentralized stablecoin option. Backed by a diversified basket of crypto collateral and real-world assets, DAI offers exposure to on-chain yield opportunities without relying on a single corporate issuer. While this decentralization reduces counterparty risk, it introduces complexity in valuation and collateral management. Treasuries with sophisticated DeFi capabilities may use DAI to optimize yield, but it requires robust monitoring of collateral ratios and oracle feeds.

Compliance and risk management checklist

Integrating stablecoin flows into treasury infrastructure requires a structured approach to regulatory adherence and operational security. As global frameworks tighten in 2026, treasury managers must prioritize verified reserve backing and strict AML protocols to mitigate institutional risk [[src-serp-4]].

Select stablecoins issued by entities with audited, real-time reserve disclosures and clear regulatory licensing. Prefer USDC for its native conversion capabilities and regulated reserve structure, ensuring the issuer meets current compliance standards.

Deploy automated identity verification tools that integrate with your existing financial infrastructure. Ensure all counterparties undergo strict Know Your Customer (KYC) checks and that transaction monitoring systems flag suspicious activity in real time.

Secure treasury assets using multi-signature wallets requiring multiple authorized approvals for transactions. This reduces single points of failure and ensures that no single individual can authorize high-value stablecoin movements without consensus.

Adhering to these steps ensures your treasury operations remain compliant with evolving global regulations while maintaining the liquidity benefits of stablecoin infrastructure.

No comments yet. Be the first to share your thoughts!