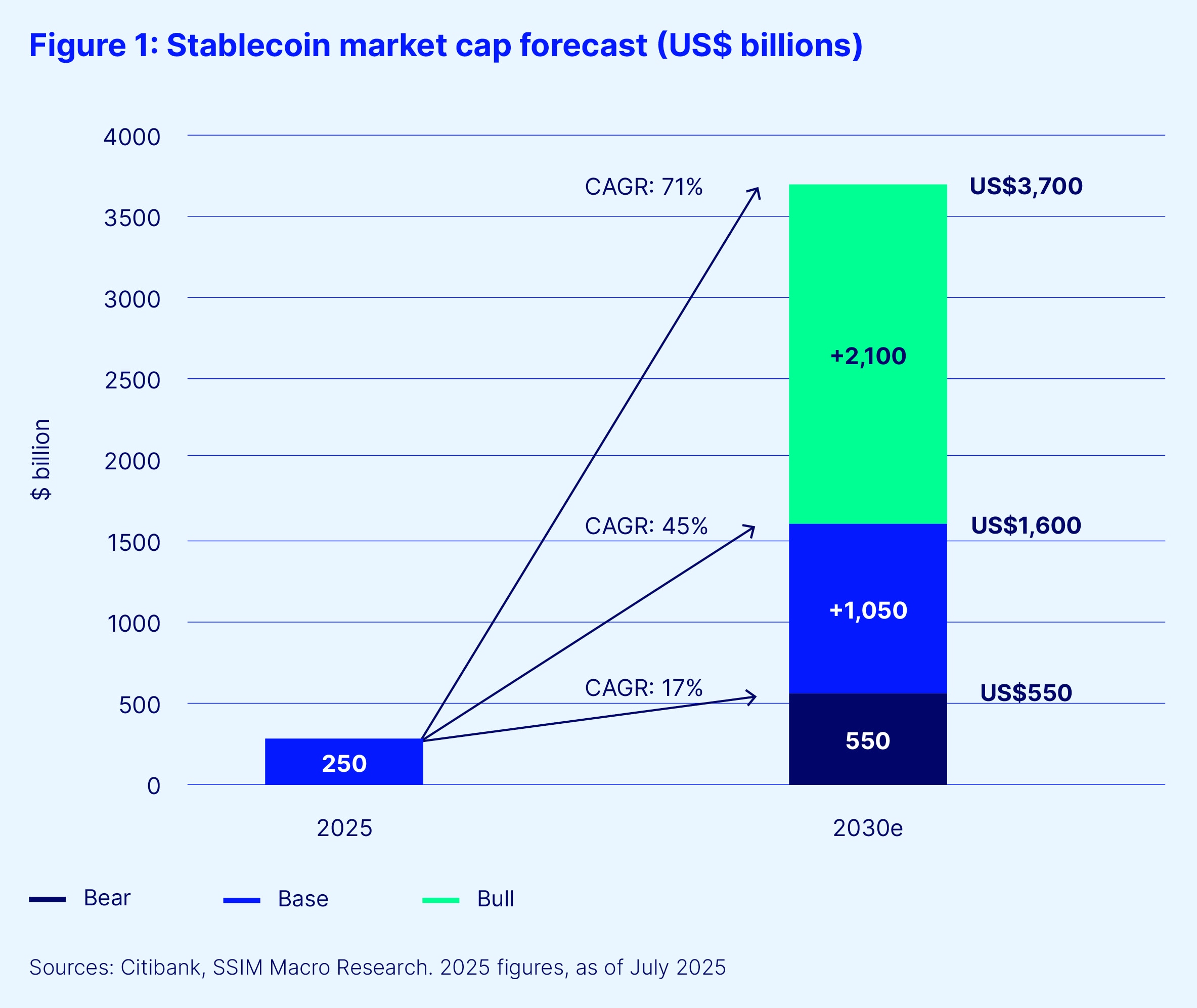

The utility shift in stablecoin flows 2026

The narrative around stablecoins has moved past speculation. In 2026, the focus is on practical utility, driven by regulatory clarity and the integration of real-world assets (RWA). Stablecoins are no longer just speculative holdings; they are becoming essential plumbing for global payments and treasury operations.

Forbes notes that 2026 continues to see considerable discussion around stablecoins, but with an increasing focus on action compared to 2025. This shift is evident in the growing volume of B2B flows, where businesses are leveraging stablecoins for faster, cheaper cross-border settlements. The infrastructure is maturing, enabling real-time liquidity that traditional banking systems struggle to match.

Regulatory frameworks are providing the necessary guardrails for institutional adoption. As rules become clearer, large-scale financial institutions are integrating stablecoins into their core operations. This trend is expected to accelerate, particularly in treasury management and global trade finance, where efficiency and transparency are paramount.

The integration of RWAs further solidifies this utility. By tokenizing real-world assets, stablecoins gain a tangible backing that appeals to conservative investors and institutions. This development not only enhances trust but also opens up new avenues for liquidity in traditionally illiquid markets.

USDC and USDT Market Share 2026

The stablecoin duopoly has solidified, but the division of labor between Circle’s USDC and Tether’s USDT has sharpened. In 2026, USDC remains the preferred settlement layer for institutional finance, while USDT dominates retail trading and emerging market liquidity. This split is driven less by technology and more by regulatory clarity and counterparty trust.

USDC’s market position is anchored by its full reserve model and direct compliance with U.S. financial regulations. For institutional players moving large volumes, the transparency of USDC’s issuance and redemption process reduces operational risk. As global stablecoin rules begin to take shape, regulatory frameworks are accelerating adoption among traditional finance firms that require audit trails and legal certainty. This environment favors USDC, which aligns closely with the evolving expectations of regulated entities.

Tether, conversely, retains a massive lead in total market capitalization, driven by its ubiquity on non-U.S. exchanges and its role as the primary trading pair for speculative assets. While USDC captures the high-value, low-frequency institutional flows, USDT handles the high-frequency, lower-value retail transactions that move billions daily across global markets. The choice between them often comes down to the user’s regulatory jurisdiction and their specific use case.

The following table compares the core metrics that define their respective roles in the 2026 market.

| Metric | USDC | USDT | Market Impact |

|---|---|---|---|

| Primary User Base | Institutions & Corporates | Retail & Traders | Determines exchange liquidity pools |

| Regulatory Alignment | High (U.S. Compliant) | Moderate (Global) | Drives institutional adoption rates |

| Reserve Transparency | Monthly Attestations | Quarterly Audits | Affects counterparty risk perception |

| Trading Volume Share | ~35% | ~65% | Sets daily settlement velocity |

| Regional Dominance | North America & EU | Asia, LatAm & Global | Defines geographic liquidity centers |

Real-World Assets and Stablecoin Demand

Tokenizing real-world assets (RWA) like US Treasuries and private credit is reshaping stablecoin utility. Instead of sitting idle as cash reserves, stablecoins are becoming the settlement layer for tokenized bonds. This shift creates a structural demand for stablecoin supply, as issuers hold underlying assets to back the tokens they distribute.

Major stablecoin issuers have already pivoted their reserve strategies. Tether (USDT) and Circle (USDC) now hold tens of billions in short-term US Treasuries. This isn't just treasury management; it's the financialization of the stablecoin itself. When an institution buys a tokenized bond, they often pay with USDC. That USDC is then converted into the underlying security, effectively locking up stablecoin liquidity in the RWA market.

This dynamic turns stablecoins into a yield-bearing asset class in their own right. The GENIUS Act has further solidified this framework by establishing clear regulatory guardrails for stablecoin issuers in the United States. With regulatory clarity, institutional capital is moving faster into tokenized markets, where stablecoins serve as the primary bridge between traditional finance and blockchain settlement.

The feedback loop is becoming self-reinforcing. As more RWAs are tokenized, the need for efficient, 24/7 settlement increases. Stablecoins provide that efficiency. Consequently, issuers are incentivized to hold more high-quality liquid assets (HQLA) to maintain trust and comply with new regulations, further deepening the link between stablecoin supply and traditional bond markets.

Market Data: USDC and USDT

The following chart illustrates the recent price stability and market behavior of the two largest stablecoins. Their peg to the US dollar remains critical for RWA settlement efficiency.

Stablecoins replace SWIFT corridors

Stablecoins are moving from speculative assets to practical infrastructure for cross-border business payments. While they represent only about 1% of global payment flows, this share has remained stubbornly flat since 2023 despite explosive growth in absolute transaction volume. This stagnation in market share masks a structural shift: enterprises are quietly migrating B2B settlements away from traditional SWIFT corridors to blockchain rails that settle in minutes rather than days.

The primary driver is liquidity efficiency. Traditional correspondent banking requires pre-funded nostro accounts in multiple currencies, tying up capital that could otherwise be deployed. Stablecoins allow firms to hold a single reserve asset and settle instantly across borders, reducing the cost of capital and eliminating the lag of intermediary bank checks. For remittances and high-frequency B2B trade, this speed translates directly into working capital optimization.

Market liquidity context

To understand the scale of this shift, it helps to look at the underlying asset stability that makes these flows possible. The reliability of USDT and USDC is the bedrock of this infrastructure.

The adoption gap

Despite the technical advantages, adoption remains concentrated in specific corridors and use cases. Traditional banking networks still dominate large-scale institutional flows due to regulatory familiarity and existing legal frameworks. However, the gap is narrowing as regulatory clarity improves in key jurisdictions, allowing more traditional financial institutions to offer stablecoin custody and settlement services alongside their legacy options.

Regulatory frameworks shaping flows

The passage of the GENIUS Act in the United States has established a definitive regulatory framework for stablecoins, transforming them from experimental assets into compliant financial instruments. This legislation provides the legal clarity that institutions require to integrate stablecoins into treasury management and cross-border settlement systems. By defining reserve requirements and operational standards, the act reduces the friction that previously hindered large-scale adoption.

Globally, regulators are moving toward harmonization to prevent arbitrage and ensure financial stability. New rules are accelerating adoption while simultaneously shaping demand for underlying assets like US debt, which backs many major stablecoins. The European Union’s MiCA regulation and ongoing efforts in the UK to finalize their own framework demonstrate a broader shift toward standardized oversight. This convergence allows capital to flow more freely across borders without encountering fragmented compliance barriers.

For institutional liquidity, these frameworks act as a signal of safety. When operators know the rules of engagement, they are more willing to lock capital into tokenized real-world assets (RWAs). The reduction in regulatory uncertainty is a primary driver for the projected growth in stablecoin volume throughout 2026.

No comments yet. Be the first to share your thoughts!