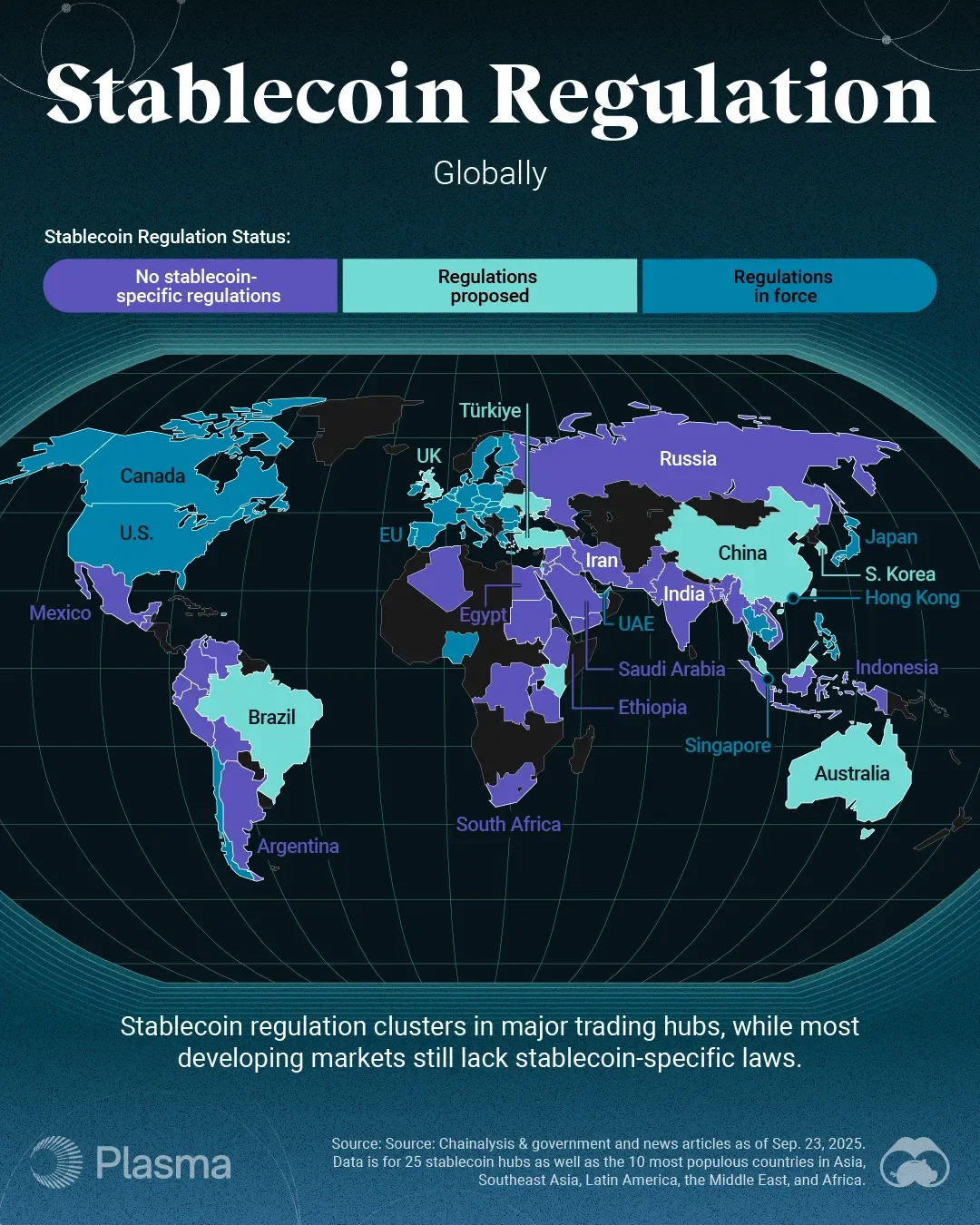

Stablecoin regulation 2026 limits to account for

The regulatory landscape for digital assets shifted decisively in 2026 with the implementation of the GENIUS Act. This legislation established the first comprehensive federal framework for payment stablecoins, moving the industry away from ambiguity toward a structured compliance model. The law directs the Treasury Department to treat permitted payment stablecoin issuers (PPSIs) as financial institutions under the Bank Secrecy Act, imposing strict anti-money laundering obligations.

The constraints on market size are explicit and significant. According to proposed rules published in the Federal Register, the upper bound for payment stablecoin issuance is capped at $250 billion in 2025, rising to $500 billion in 2026. These caps are designed to prevent systemic risk while allowing the market to mature under federal oversight. Issuers must now navigate a rigorous approval process to maintain their status.

Beyond issuance limits, the 2026 regulatory environment is defined by a push for yield-bearing stablecoins. Users increasingly expect digital dollars to produce passive returns through tokenized Treasury exposure and on-chain lending markets. This trend reflects a broader demand for utility in stablecoins, moving them from mere store-of-value mechanisms to active financial instruments. The new guidelines aim to balance this innovation with the necessary consumer protections and liquidity safeguards required by federal regulators.

Stablecoin regulation 2026 choices that change the plan

The GENIUS Act, enacted in July 2025, establishes a federal framework for payment stablecoins. The Treasury and OCC are now finalizing rules that treat Permitted Payment Stablecoin Issuers (PPSIs) as financial institutions under the Bank Secrecy Act. This shift imposes strict anti-money laundering obligations and reserve requirements that fundamentally change how issuers operate.

Issuers face a clear choice between scale and compliance cost. The proposed rules cap payment stablecoin issuance at $250 billion in 2025 and $500 billion in 2026. While this provides a clear runway for growth, it forces issuers to prioritize regulatory efficiency over aggressive expansion. Smaller issuers may find the compliance burden too high, consolidating the market around fewer, larger players.

Yield-bearing features add another layer of complexity. The 2026 trend shows users expecting passive returns through tokenized Treasury exposure. However, current regulations separate the payment function from the yield function. Issuers must structure their products to ensure the stablecoin itself remains a stable payment rail, while yield mechanisms are handled through separate, compliant financial channels.

| Feature | GENIUS Act Compliance | Pre-2025 Practice |

|---|---|---|

| Reserve Assets | High-quality liquid assets (HQLA) | Mixed commercial paper, corporate debt |

| Oversight | Federal regulator (OCC/Fed) | State charters or self-regulation |

| BSA/AML | Full financial institution status | Varying, often lighter standards |

| Issuance Cap | $500 billion (2026) | No federal cap |

The market is already reacting to these regulatory shifts. The technical chart for USDT/USDT shows how liquidity flows are adjusting to the new compliance landscape. Traders are watching volume patterns closely as issuers migrate reserves to meet the new HQLA standards.

PriceWidget symbol="USDT" assetType="crypto" tvSymbol="BINANCE:USDTUSDT" />

How to Evaluate Stablecoin Issuers Under the 2026 Framework

The GENIUS Act shifts stablecoin regulation from a patchwork of state laws to a unified federal system. The Treasury’s proposed rule, published in the Federal Register, establishes the baseline for compliance. For issuers and investors, the new standard focuses on reserve transparency, redemption rights, and AML alignment. Use this framework to assess whether a stablecoin meets the new federal requirements before allocating capital.

Payment stablecoins must hold reserves in high-quality liquid assets. The 2026 guidelines prioritize short-term U.S. Treasury securities and cash. Avoid issuers relying heavily on commercial paper or private credit, as these assets introduce liquidity risk during market stress. Check the issuer’s monthly attestation reports to confirm the ratio of cash to treasury holdings.

Under the GENIUS Act, issuers must guarantee on-demand redemption at par value. Evaluate the speed and cost of withdrawals. Legitimate issuers process redemptions within one business day without hidden fees. If an issuer imposes delays or penalties for large withdrawals, it likely violates the new federal redemption standards.

Permitted Payment Stablecoin Issuers (PPSIs) are now subject to Bank Secrecy Act obligations. This means they must implement robust anti-money laundering (AML) programs and report suspicious activities. Look for issuers that publish clear KYC (Know Your Customer) policies and cooperate with federal law enforcement. Non-compliance can lead to immediate revocation of federal charters.

The 2026 framework sets upper bounds for stablecoin issuance: $250 billion in 2025 and $500 billion in 2026. Issuers approaching these caps may face stricter scrutiny or temporary freezes on new minting. Investors should track total supply metrics to avoid assets that might be forced to contract rapidly, which could trigger price instability.

Spotting Weak Options in 2026 Stablecoin Compliance

The GENIUS Act framework creates a clear regulatory line: only Permitted Payment Stablecoin Issuers (PPSIs) may issue stablecoins for U.S. persons. However, many projects still rely on weak options that risk non-compliance. The most common mistake is treating regulatory guidance as optional rather than mandatory. Issuers must now treat stablecoin operations as financial institutions under the Bank Secrecy Act, imposing strict anti-money laundering obligations.

Another misleading claim is the assumption that all stablecoins are equal. The new rules distinguish payment stablecoins from other digital assets. Yield-bearing stablecoins are expanding, but they must navigate separate compliance layers. Projects that ignore these distinctions face significant regulatory hurdles.

To stay compliant, focus on concrete checks. Verify your issuer status, ensure proper reserve backing, and implement robust AML procedures. Avoid vague promises about decentralization as a shield against regulation. The SEC and Treasury are watching closely, and the window for adjustment is closing.

Stablecoin regulation 2026: what to check next

The regulatory landscape for digital assets is shifting rapidly as new federal guidelines take shape. Below are answers to the most common questions regarding the GENIUS Act and its impact on global liquidity.

No comments yet. Be the first to share your thoughts!