Market shifts in stablecoin flows 2026

The stablecoin market in 2026 has undergone a structural pivot from retail speculation to institutional utility, particularly in cross-border payments. This transition is not merely a change in user demographics but a fundamental shift in how capital moves across borders. Traditional finance is increasingly integrating stablecoins into its settlement layers, driven by the need for speed, transparency, and cost efficiency in international transactions.

Data from the International Monetary Fund (IMF) indicates that stablecoin markets are now deeply linked to traditional finance. The spillover effects on foreign exchange (FX) markets are significant, affecting currency stability and monetary policy transmission. As institutions adopt stablecoins for treasury management and cross-border settlements, the volume of flows has surged, reflecting a growing confidence in these digital assets as a reliable medium of exchange rather than just a speculative vehicle.

The rise in stablecoin holdings underscores this institutional adoption. According to the BVNK Stablecoin Utility Report 2026, half of stablecoin holders increased their holdings in the last 12 months, with over 56% planning to acquire more. This trend is driven by businesses seeking to reduce the friction and costs associated with traditional correspondent banking. By holding stablecoins, institutions can settle transactions in real-time, bypassing the delays and fees inherent in the SWIFT network.

This shift has profound implications for the global financial system. As stablecoin flows increase, they are reshaping the landscape of cross-border payments, offering a faster and more efficient alternative to traditional methods. However, this growth also brings regulatory challenges, as central banks and financial authorities grapple with the implications of stablecoin adoption on monetary sovereignty and financial stability. The IMF’s findings highlight the need for a coordinated regulatory approach to manage these spillovers and ensure that the integration of stablecoins into the global financial system is both safe and sustainable.

Institutional adoption drivers

The transition of stablecoins from speculative assets to functional payments infrastructure marks a structural shift in global finance. By 2026, institutional adoption is no longer driven by speculation but by the tangible efficiency gains stablecoins offer over traditional banking rails, particularly in business-to-business (B2B) payments and treasury operations. This shift reflects a broader re-evaluation of capital velocity and settlement finality.

Stablecoins are increasingly functioning as the underlying plumbing for cross-border B2B flows. Traditional correspondent banking networks involve multiple intermediaries, each adding layers of friction, cost, and time. Stablecoins bypass this fragmented architecture, enabling near-instant settlement across jurisdictions. This efficiency is critical for multinational corporations managing complex supply chains where working capital is tied up in transit. As noted in industry analyses, the focus has moved from theoretical discussions to practical implementation, with enterprises leveraging stablecoins to reduce the time value of money lost in traditional clearing cycles.

Treasury operations represent another primary driver for institutional adoption. Corporations are utilizing stablecoins to optimize liquidity management, allowing for real-time movement of funds without the delays inherent in traditional wire transfers. This capability provides greater visibility and control over global cash positions. The regulatory environment and the demand for transparency are shaping how institutions deploy these tools. Trust remains paramount; therefore, institutions are prioritizing stablecoins backed by high-quality liquid assets and subject to rigorous auditing, aligning with the growing emphasis on regulatory compliance and economic incentives.

The integration of stablecoins into corporate finance is also supported by the broader digital asset ecosystem. Major payment processors and financial technology firms are building infrastructure that allows seamless integration of stablecoin payments into existing enterprise resource planning (ERP) systems. This interoperability reduces the technical barrier to entry, enabling institutions to leverage the speed of blockchain settlement while maintaining the stability of fiat-pegged assets. The result is a hybrid financial landscape where digital assets complement traditional banking, offering institutions a more efficient, transparent, and cost-effective method for managing global transactions.

Regulatory landscape and compliance

The 2026 regulatory environment has shifted from speculative inquiry to rigid compliance, fundamentally altering how stablecoins function in cross-border payments. The European Union’s Markets in Crypto-Assets (MiCA) regulation has established the first comprehensive legal framework for stablecoin issuers, creating a new category of "permitted stablecoin issuers" that must adhere to strict reserve and governance standards. This regulatory clarity has accelerated institutional adoption, as banks and payment processors can now integrate stablecoins with known legal boundaries. The Payments Association notes that these new global rules are reshaping payment infrastructure by reducing regulatory uncertainty, which in turn is driving demand for US debt instruments as reserve backing.

In the United States, the regulatory approach remains fragmented but is coalescing around federal oversight of money transmission and securities laws. While a unified federal stablecoin bill has yet to pass, major financial institutions are aligning with existing frameworks from the Office of the Comptroller of the Currency and the Federal Reserve. This patchwork of state and federal requirements forces issuers to implement robust know-your-customer (KYC) and anti-money laundering (AML) protocols that go beyond traditional banking standards. The result is a higher barrier to entry, which consolidates the market among well-capitalized issuers capable of absorbing compliance costs.

Cross-border flow compliance has become the primary operational challenge for issuers. Traditional correspondent banking networks are being supplemented by stablecoin rails, but these rails must still satisfy the Bank Secrecy Act and international sanctions lists. The IMF has emphasized that stablecoin issuers must maintain transparent, real-time proof of reserves to prevent systemic risk. This requirement has led to the adoption of on-chain auditing tools that provide continuous verification of backing assets, a significant departure from the quarterly attestation models used in traditional finance.

The convergence of these regulatory pressures is reshaping the competitive landscape. Issuers that prioritize regulatory compliance over speed of deployment are gaining market share among institutional clients who require audit trails and legal recourse. As the UK finalizes its own stablecoin framework to align with MiCA, global issuers are standardizing their compliance operations to serve multiple jurisdictions simultaneously. This harmonization reduces friction for cross-border payments, allowing financial institutions to move capital across borders with the speed of blockchain technology and the legal certainty of traditional banking.

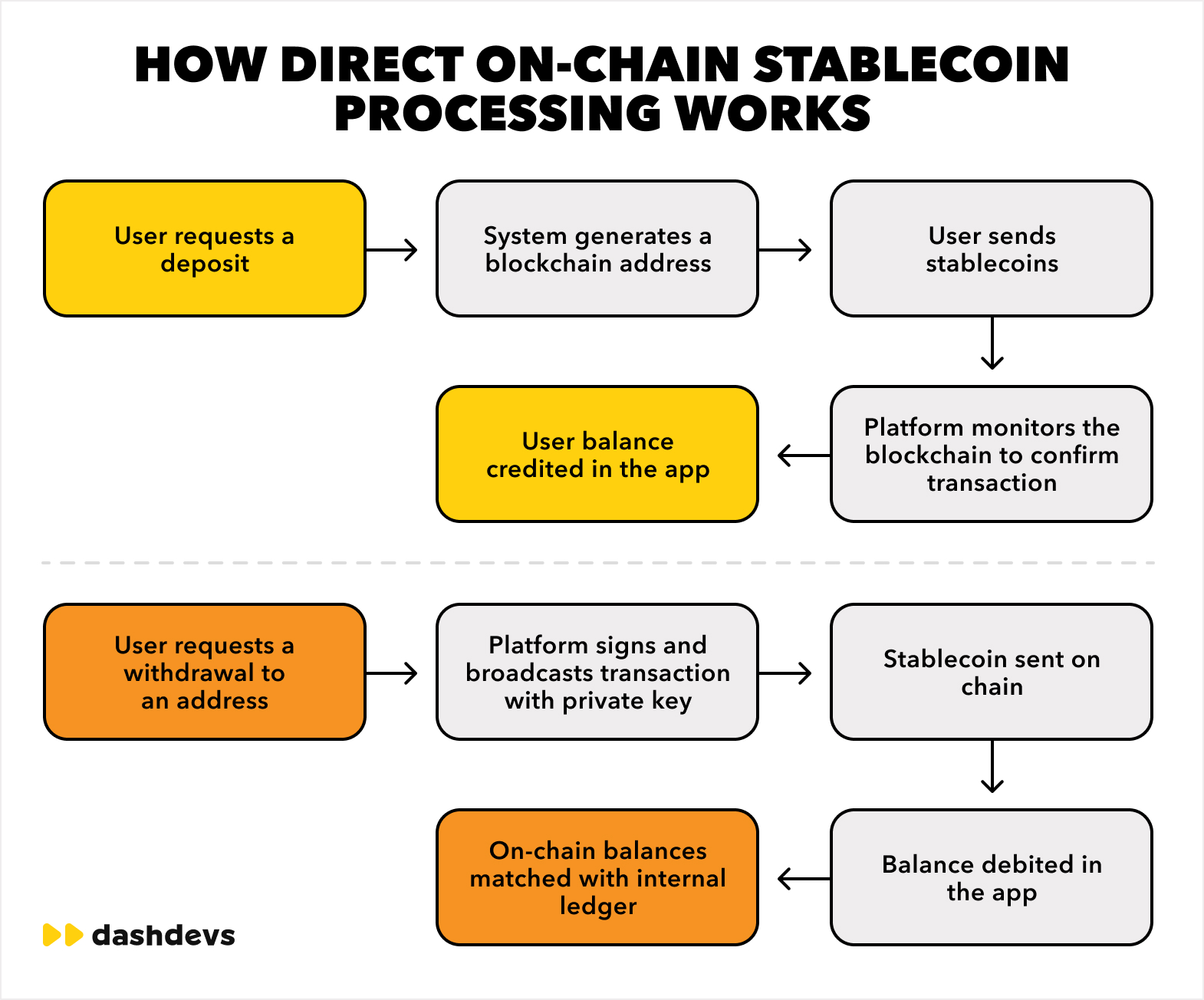

Cross-border payment infrastructure

The migration of cross-border payments from traditional correspondent banking to stablecoin rails represents a fundamental shift in financial infrastructure. This transition is driven by the need to reduce friction, lower costs, and increase transparency in international settlements. While the SWIFT network remains the backbone of global interbank communication, its underlying settlement layers often rely on pre-funded nostro/vostro accounts, which tie up capital and introduce latency.

Stablecoins offer a different operational model. By utilizing blockchain technology, they enable near-instant settlement on a finality basis, eliminating the need for multiple intermediary banks. This efficiency is particularly valuable for high-frequency trading, remittances, and supply chain finance, where speed and cost are critical competitive advantages. The following table compares the operational characteristics of stablecoin rails against traditional banking systems.

| Feature | Stablecoin Rails | Traditional Banking |

|---|---|---|

| Settlement Time | Seconds to minutes | 1-5 business days |

| Cost Structure | Low, network-based fees | High, intermediary fees |

| Capital Efficiency | High, no pre-funding | Low, nostro accounts |

| Transparency | Real-time ledger access | Limited, batch processing |

| Accessibility | 24/7 global access | Banking hours, regional |

Regulatory frameworks are rapidly evolving to accommodate this shift. The IMF and various central banks are closely monitoring the integration of stablecoins into the global payment system, emphasizing the need for robust oversight to prevent systemic risks. As 2026 progresses, the convergence of regulatory clarity and technological maturity is accelerating the adoption of stablecoins for institutional cross-border payments.

Key stablecoins for 2026

The 2026 institutional landscape is defined by the divergence between trading liquidity and settlement utility. Tether (USDT) remains the dominant vehicle for cross-border liquidity, capturing the majority of volume in emerging markets and OTC desks. Its dominance is structural, driven by deep integration with global exchanges and a reserve composition that prioritizes high-quality short-term U.S. Treasury bills.

USDC, issued by Circle, serves as the primary settlement layer for regulated institutional flows. Its transparency and regulatory alignment make it the preferred choice for corporate treasuries and payment processors operating within strict compliance frameworks. The distinction is clear: USDT is the liquidity engine, while USDC is the compliance rail.

| Asset | Issuer | Primary Institutional Use | Regulatory Stance |

|---|---|---|---|

| USDT | Tether | Cross-border liquidity & OTC trading | High volume, evolving reserve audits |

| USDC | Circle | Settlement & corporate payments | Fully reserved, regulated issuer |

Emerging entrants like PYUSD and EURC are carving out niche roles, particularly in specific jurisdictions and fiat pairs. However, the concentration of market share in USDT and USDC creates a duopoly that institutions must navigate carefully. Risk management strategies now focus on diversifying custody across these primary rails to mitigate issuer-specific exposure.

The institutional preference for these assets is not merely about price stability but about the reliability of the underlying payment rails. As central banks explore digital currencies, private stablecoins currently fill the immediate void for instant, programmable settlement. This dynamic reinforces the necessity of understanding the specific operational mechanics of each major stablecoin.

No comments yet. Be the first to share your thoughts!