USDC (USD Coin) has rapidly emerged as the primary stablecoin underpinning Base, Coinbase’s Layer-2 blockchain. Unlike bridged stablecoins, which introduce additional risk and complexity, native USDC Base is issued directly on the network and fully backed by Circle’s U. S. dollar reserves. This distinction is more than technical - it is foundational to the security, liquidity, and real-world utility that Base offers to users and developers.

Native USDC: The Trust Anchor for Base

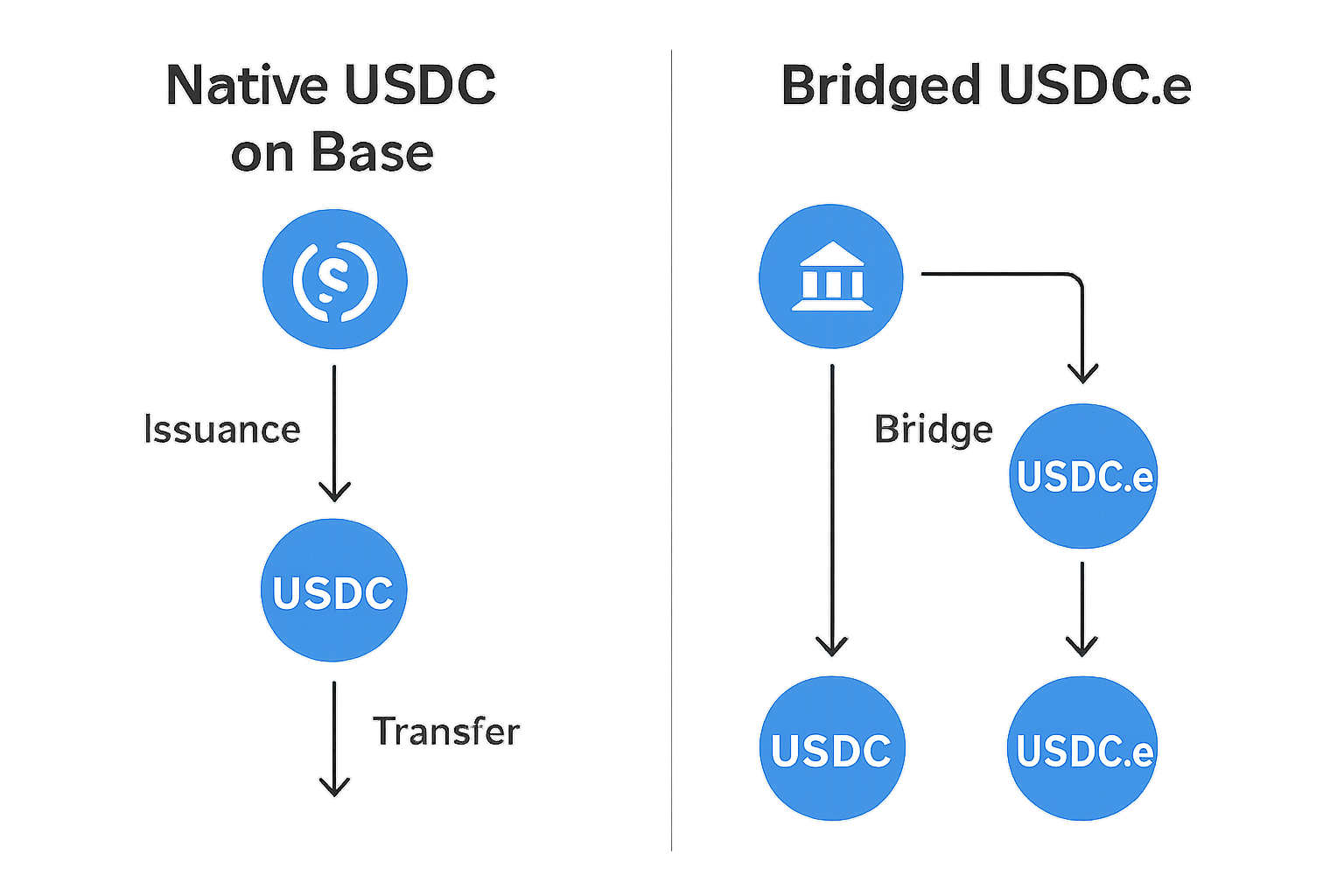

Understanding the difference between native and bridged stablecoins is essential for anyone navigating DeFi or considering large-scale integrations. Native USDC Base tokens are minted directly by Circle on the Base network, meaning each token is always redeemable 1: 1 for U. S. dollars through Circle. In contrast, bridged versions like USDC. e are created by third-party protocols that lock up native tokens on another chain and issue a representation on Base. These representations are not directly redeemable from Circle and carry smart contract and custodial risks that can distort price data and undermine user trust.

This separation has led to market consolidation around official, native tokens, as highlighted by ongoing movements away from bridged assets across DeFi. Accurate price discovery and reliable liquidity depend on this clarity - which is why platforms like CoinGecko list native and bridged stablecoins separately.

Base Stablecoin Liquidity: $500 Million and Deployed

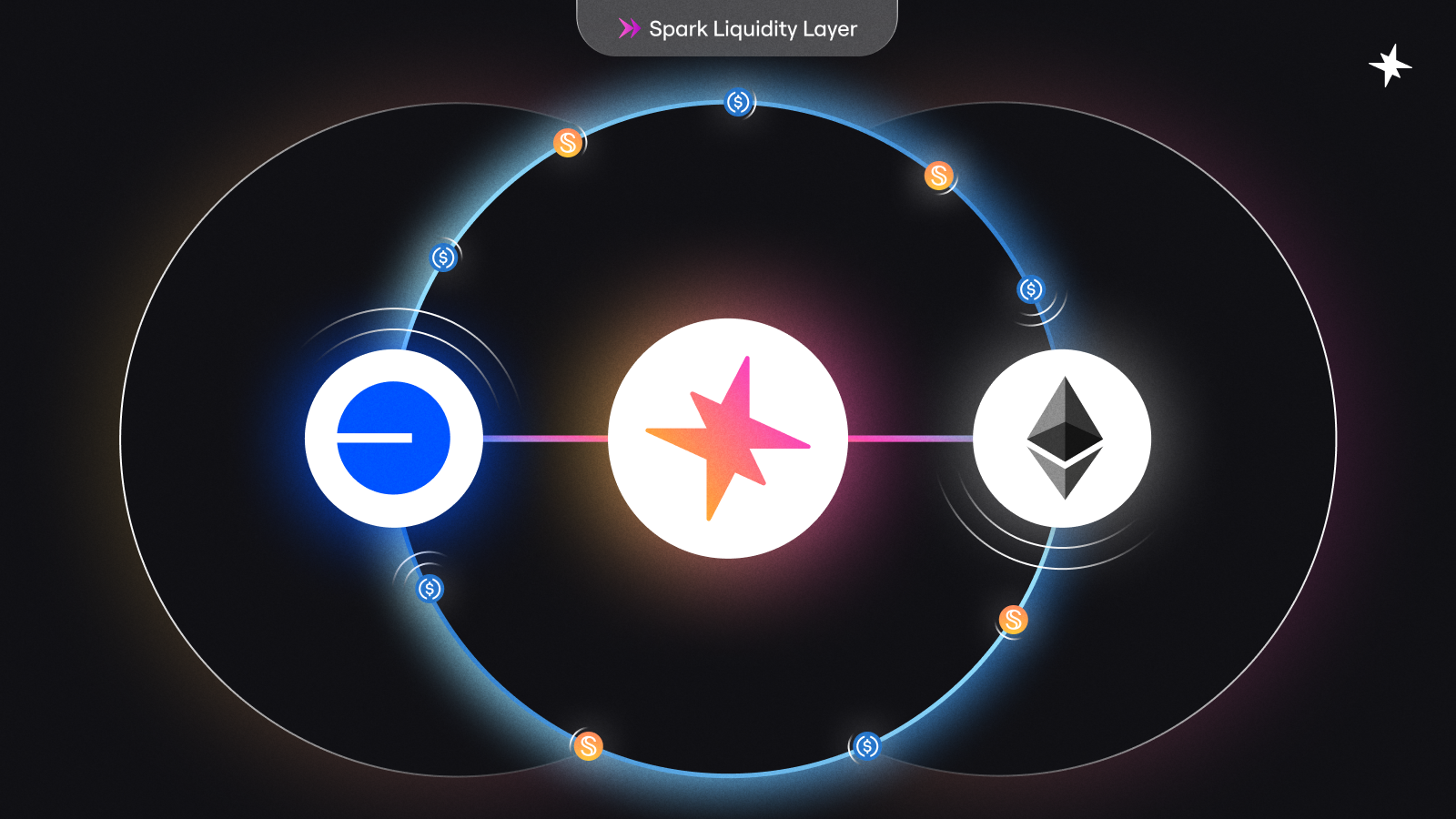

The impact of USDC Base’s native integration is immediately visible in liquidity metrics. The Spark Liquidity Layer, via MorphoLabs’ USDC Vault, has deployed over $500 million in USDC liquidity on Base. This deep pool enables efficient trading pairs, robust lending markets, and a foundation for new DeFi protocols to launch with confidence in their settlement layer.

This scale of liquidity not only attracts sophisticated traders but also lowers slippage for retail users and expands opportunities for arbitrage across chains. It positions Base as a go-to network for both institutional capital flows and grassroots adoption - a rare combination in the current market landscape.

Key Benefits of Native USDC on Base vs Bridged Alternatives

- Direct 1:1 USD Redemption Backed by Circle: Native USDC on Base is issued and managed directly by Circle, ensuring each token is fully backed by U.S. dollar reserves and redeemable 1:1 for USD. In contrast, bridged USDC (such as USDC.e or USDbC) is not issued by Circle and cannot be directly redeemed for dollars, introducing additional counterparty and liquidity risks.

- Enhanced Security and Regulatory Clarity: Native USDC benefits from Circle's compliance with U.S. regulatory standards, offering users greater transparency and legal assurance. Bridged alternatives rely on third-party bridge protocols, which can be vulnerable to smart contract exploits and lack regulatory oversight.

- Superior Liquidity and DeFi Integration: Base has attracted significant native USDC liquidity, with over $500 million deployed via the Spark Liquidity Layer and MorphoLabs. This deep liquidity supports efficient trading, lending, and borrowing, whereas bridged tokens often suffer from fragmented liquidity and higher slippage.

- Seamless On-Chain Utility and Ecosystem Adoption: Native USDC is fully integrated into Base's ecosystem, enabling features like Coinbase's USDC lending (with yields up to 10.8% via Morpho) and direct Shopify USDC payments. Bridged USDC may face limited support and compatibility issues across platforms.

- Accurate Price Data and Market Transparency: Exchanges and data aggregators (e.g., CoinGecko) list native USDC separately from bridged versions to avoid price distortions. Native USDC provides reliable market data, while bridged tokens can introduce inaccurate pricing and confusion for users.

On-Chain Utility: From Lending to Real-World Payments

The utility of USDC DeFi integration extends far beyond trading or holding. Coinbase’s recent move to offer direct USDC lending within its app - allowing yields up to 10.8% via Morpho - illustrates how deeply integrated stablecoin functionality has become within the Base ecosystem. Users can lend their USDC to borrowers directly on-chain, earning competitive returns while maintaining exposure to a fully-backed dollar asset.

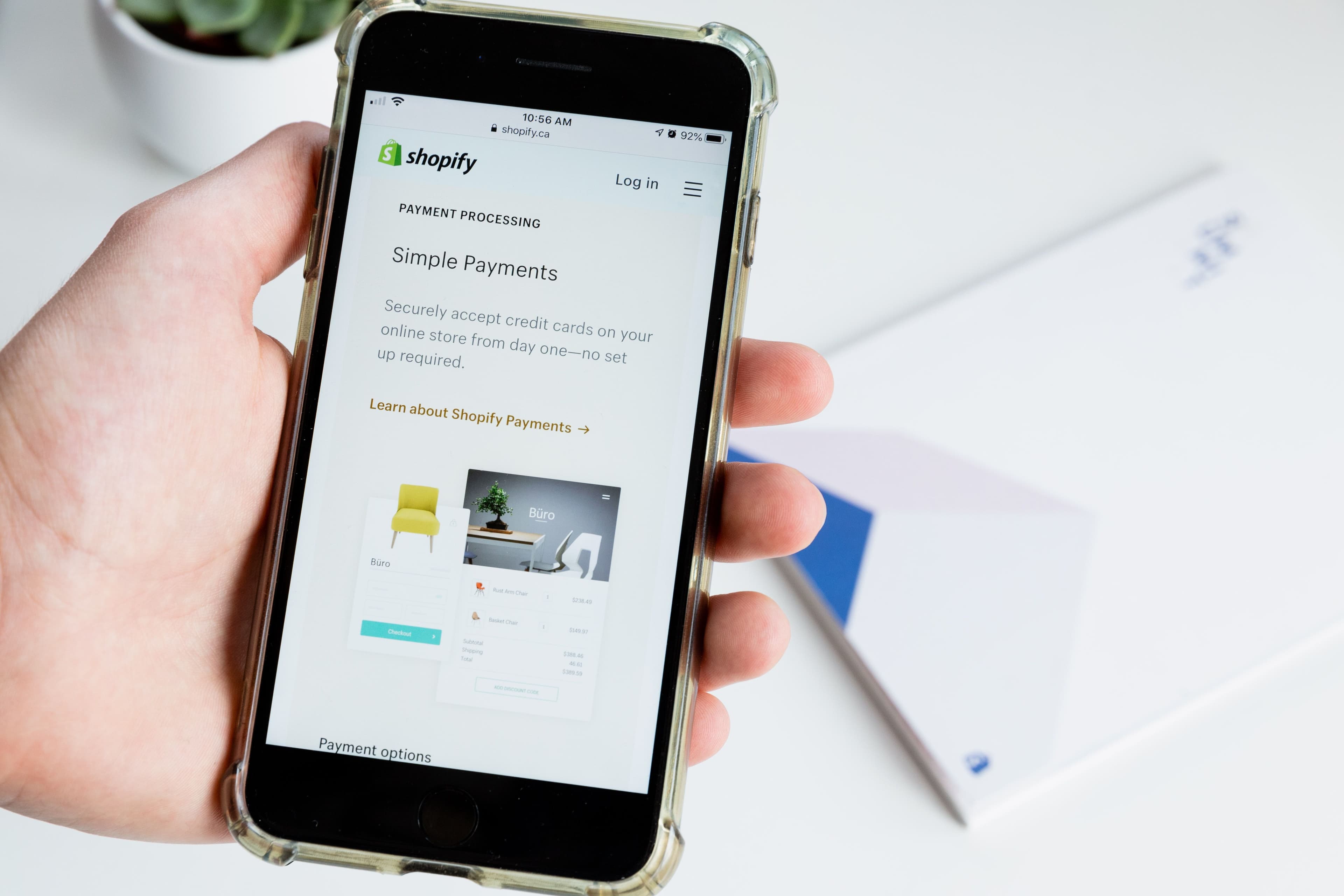

The momentum isn’t limited to financial primitives. Shopify merchants can now accept Base on-chain payments using USDC at checkout, marking a milestone in mainstream crypto adoption that bridges DeFi with real-world commerce. This seamless payment experience leverages the speed, low fees, and stability of native USDC - attributes that would be compromised if relying solely on bridged or synthetic alternatives.

The Road Ahead for Stablecoin Adoption on Base

The convergence of secure issuance, ample liquidity, and practical utility cements USDC as the backbone of the Base network. As adoption accelerates among both developers and end-users, expect further innovation in payment rails, yield products, and cross-chain interoperability anchored by this robust stablecoin infrastructure.

Looking forward, the implications for stablecoin adoption on Base are profound. By prioritizing native issuance, Base sidesteps the pitfalls that have plagued other ecosystems reliant on bridged assets, namely, fragmented liquidity, smart contract vulnerabilities, and a lack of regulatory clarity. This strategic focus is already translating into tangible network effects: newer DeFi protocols are listing native USDC as their default stablecoin, and liquidity mining incentives are increasingly denominated in USDC Base rather than wrapped or bridged variants.

For developers, the presence of deep, reliable Base stablecoin liquidity means they can build sophisticated financial products, ranging from automated market makers to collateralized lending platforms, without worrying about exit liquidity or sudden depegs. For users, the assurance that their stablecoin is always redeemable 1: 1 for dollars through Circle fosters a level of trust rarely seen in the DeFi space. This trust is essential as more mainstream applications, such as payroll, remittances, and merchant payments, go live on-chain.

Why Native Matters: Security, Transparency, and Growth

The security profile of native USDC Base is a decisive advantage. Unlike bridged tokens, which rely on third-party custodians or complex smart contracts, native USDC benefits from direct oversight by Circle and clear regulatory frameworks. This minimizes systemic risk and enables institutional participants to engage with Base-based DeFi confidently. Transparency is further enhanced by real-time attestations of USDC reserves, allowing anyone to independently verify backing and circulation.

Growth prospects for USDC Base are amplified by its utility as a settlement asset. As more dApps integrate native USDC for everything from NFT marketplaces to prediction markets, the velocity of money within the Base ecosystem increases. This not only drives fee revenue for validators but also attracts new capital seeking both yield and stability, a virtuous cycle that entrenches USDC’s role as Base’s monetary standard.

Key Use Cases Driving USDC Adoption on Base

- Decentralized Finance (DeFi) Protocols: USDC provides deep liquidity for leading DeFi platforms on Base, enabling efficient trading, lending, and borrowing. Notably, Spark Liquidity Layer has deployed over $500 million in USDC liquidity through its USDC Vault on Base via MorphoLabs, powering a wide range of financial services.

- On-Chain USDC Lending via Coinbase: Coinbase users can now lend USDC directly within the Coinbase app, with yields up to 10.8% through on-chain integration with Morpho on Base. This seamless lending experience brings DeFi yields to mainstream users in a secure, regulated environment.

- Merchant Payments with Shopify: Shopify merchants can accept USDC payments directly through their storefronts on the Base network. This integration enables stable, fast, and low-cost transactions, advancing stablecoin adoption in everyday e-commerce.

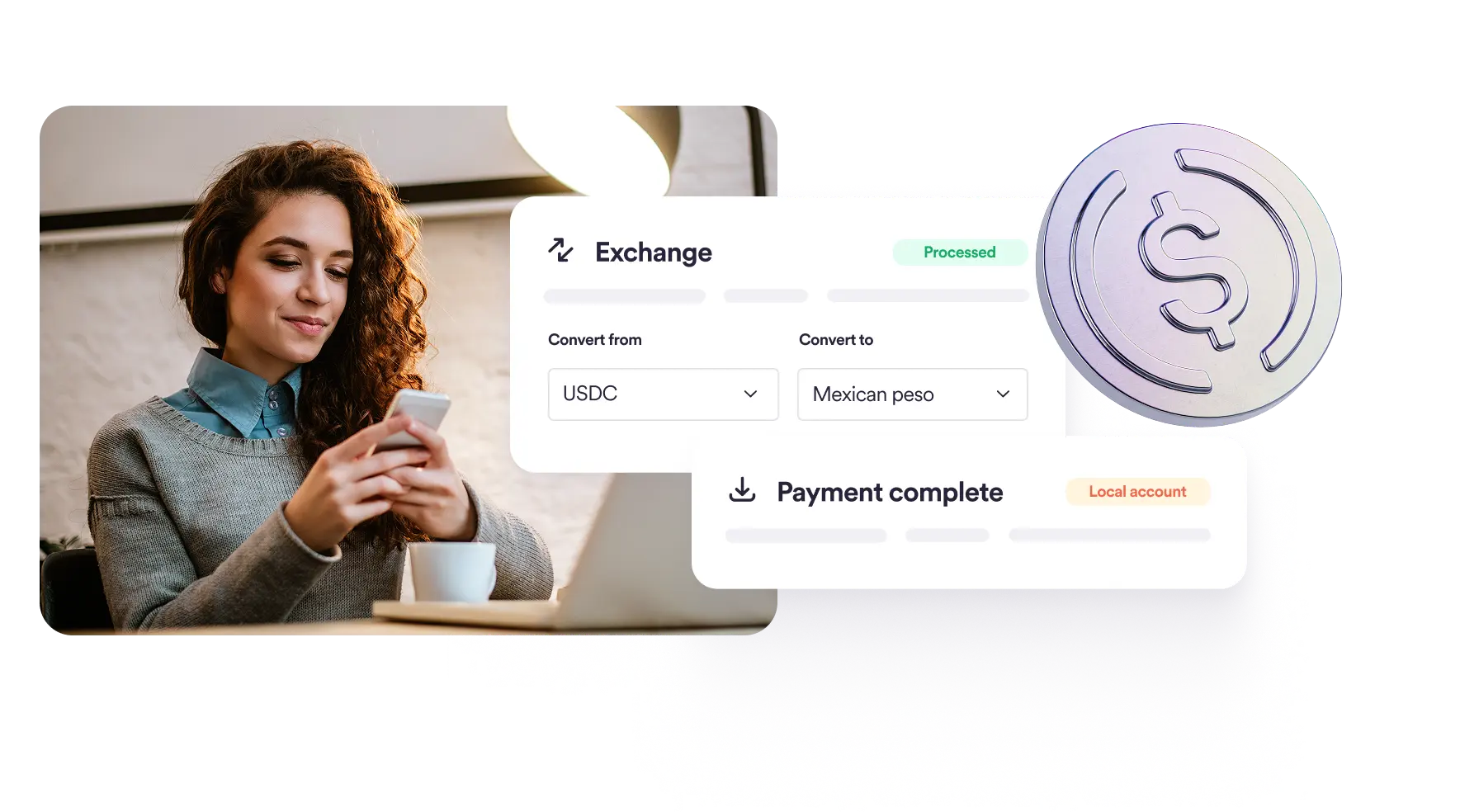

- Remittances and Peer-to-Peer Transfers: The native issuance of USDC on Base allows for instant, low-fee cross-border payments and peer-to-peer transfers, providing a stable alternative to traditional remittance channels.

- On-Chain Payroll and Business Payments: USDC's stability and programmability on Base make it ideal for on-chain payroll, invoicing, and business-to-business (B2B) payments, streamlining operations for Web3-native organizations.

The shift toward native assets is also influencing cross-chain strategies. As interoperability protocols mature, native USDC can serve as a universal settlement layer across multiple L2s and even non-EVM chains. This positions Base at the center of a future where capital moves frictionlessly between apps, networks, and real-world endpoints, all denominated in a trusted digital dollar.

Ultimately, the data is clear: USDC’s native integration, robust liquidity foundation, and expanding suite of on-chain utilities make it indispensable to the Base network’s growth trajectory. As more users demand security and seamless experiences, and as regulators scrutinize stablecoins more closely, expect native USDC to remain at the core of both DeFi innovation and mainstream adoption on Base.

No comments yet. Be the first to share your thoughts!